Pursuing Comprehensive Reform of Japan’s Social Security and Taxation Systems

Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Statistically speaking, Japan’s fiscal situation is the worst of all the member countries of the Organization for Economic Cooperation and Development.

Although Japan’s national budget for fiscal 2012 totaled ¥90.3 trillion, Japan had only ¥42.3 trillion in tax revenue. The ¥44.2 trillion shortfall was made up by issuing government bonds. On top of this, the unusual measure was taken of issuing a government compensation bond to cover the ¥2.6 trillion allocated for pension payments in the budget. Since this will have to be paid back in the future, it essentially amounts to an additional new bond issued. This marks the fourth consecutive year in which new government debt has outstripped tax revenue. On top of this, the outstanding balance of Japan’s national debt is set to exceed 219% of the nation’s total GDP in 2012, according to OECD forecasts. This level of indebtedness surpasses that of Greece and places Japan dead last among the G7 countries, well ahead of the 128% of second-place Italy.

A key factor underlying Japan’s fiscal crisis is the rising expenditure on social security such as pensions and medical and nursing care as a result of a graying population. Average life expectancy in Japan is the highest in the world, at 83, and the number of elderly people increases year after year. As of 2012, there are 2.4 people aged 20 to 64 to support every person 65 or older, but if present trends continue there will only be 1.3 people of working age for each person aged 65 or older in 2050. Japan can expect to face an extremely challenging social situation where each young person has to support one elderly person. The result of this will be a ¥1 trillion increase every year in social security expenditures.

The budget for social security programs is part of a permanent system, and is consumed by present-day generations. The fiscal principle is to cover these expenditures with permanent sources of revenue. It is highly unusual to issue government debt to fund these programs, shifting the burden to future generations. But Japan has become dependent on new bonds as a way of putting off the task of securing proper sources of budget revenue.

Japan Must Get Its Fiscal House in Order

In 2010, individual financial assets totaled ¥1,481 trillion, and 95% of all national debt was in the hands of Japanese nationals. The country also has a favorable balance of trade and a current account surplus. There is room to increase taxes—the current rate of the consumption tax is low, at just 5%. Japan is currently able to borrow cheaply, with the interest on 10-year bonds having dipped below 1% following the influx of money into Japan since the Euro crisis. These factors have led some to argue that Japan’s fiscal situation is not as dire as the statistics would suggest.

However, once housing loan obligations are deducted from the total, those household financial assets come to only ¥1,100 trillion. Meanwhile, government debt has exceeded the ¥1,000-trillion mark and continues to rise. And in 2011, as a result of factors that include the impact from the Great East Japan Earthquake, Japan’s balance of trade slipped into the red for the first time in 31 years. Its current account surplus is shrinking. Every year the country’s population gets older, and its fiscal situation is becoming worse than that of Greece. Japan has no room for complacency. Even Italy, despite its primary-balance surplus, was forced by the markets to get its finances in order. Silvio Berlusconi resigned, and the new government has pushed through a tough regime of austerity measures including an increase in the rate of the value-added tax. With the future of Japan’s social-security system in doubt, the International Monetary Fund, OECD, and credit rating agencies have warned the country that it needs to take immediate measures to improve its fiscal health.

Recognizing this need to get Japan’s fiscal house in order, Prime Minister Asō Tarō, who headed the coalition government of the Liberal Democratic Party and New Kōmeitō Party from 2008 to 2009, introduced a supplementary provision of the Tax System Reform Act of fiscal 2009. This stipulated that a debate would be held by the end of fiscal 2011 on legal measures needed for a comprehensive reform of the tax and social security systems.

Under Noda Yoshihiko, the present cabinet has adhered to the provisions of this law and reached an agreement on the content of the reforms. This is currently being formulated into a bill that the government plans to submit to the Diet in March.(*1) This legislation is part of major administrative reforms that also include reducing the number of lower-house Diet seats and cutting the civil service salaries.

Public Opinion Backs Reform

Most people in Japan recognize that if the current situation continues it will be difficult to fund the nation’s social security system, and understand the need for a consumption tax hike to secure revenue toward this end.

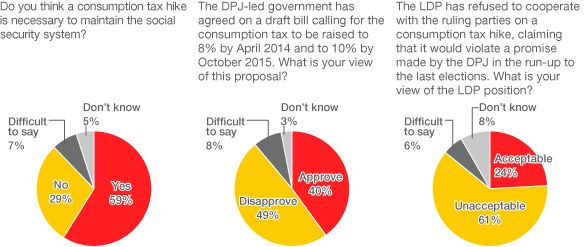

In a public opinion survey conducted by the Nikkei (published on February 20, 2012), the following views were expressed regarding how to maintain the social security system:

(1) Of the respondents, 59% said the consumption tax should be raised; 29% thought an increase was unnecessary.

(2) The proposal to increase the consumption tax to 8% by April 2014 and then to 10% by October 2015 was supported by 40% and opposed by 49%.

(3) The LDP stance of refusing to cooperate with the ruling parties to raise the consumption tax, on the grounds that this would violated the promises made by the Democratic Party of Japan in its election manifesto, was found unacceptable by 61% of those surveyed, and supported by just 24%.

Partly as a result of this and similar polls, many newspapers and other media outlets are calling on the government and the ruling and opposition parties to hold talks on the issue without delay in order to start the integrated reforms of the taxation and social security systems as soon as possible.

But there is still opposition to reform within the ruling party itself, and there has been little progress on cooperation with the opposition. But with the future of social security in peril, and Japan’s finances mired in crisis, the present generation has a duty to act to ensure that Japan avoids the fate that has befallen Greece, rather than passing the problem on to future generations.

The government needs to do more PR work to explain the issue to the public. There needs to be a serious and thorough debate in the Diet. And then the government needs to move ahead with integrated reform of the country’s tax and social security systems. This is the only way for the country to ensure the stability of social security and restore fiscal health, thereby restoring Japan’s credibility. (February 2, 2012)

(Originally written in Japanese.)

(*1) ^ The draft was submitted on March 30. As of May 2012, the debate continues.—Ed.

social security consumption tax Greece fiscal deficit OECD trade balance revenue source primary balance Prime Minister Aso comprehensive reform of social security and taxation political reform