China’s Resource-Consuming Economy Reaches Turning Point

Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

China’s Slowdown Began in 2014

At the start of 2016 two issues surfaced in the world economy: yet another downward revision of the outlook for resource prices and, on the financial side, the settlement of bad debts. Investors are shying away from stock-market risks, and even in advanced economies the market capitalization of companies continues to shrink. Recognition is growing globally that the source of these uncertainties in the world economy is China.

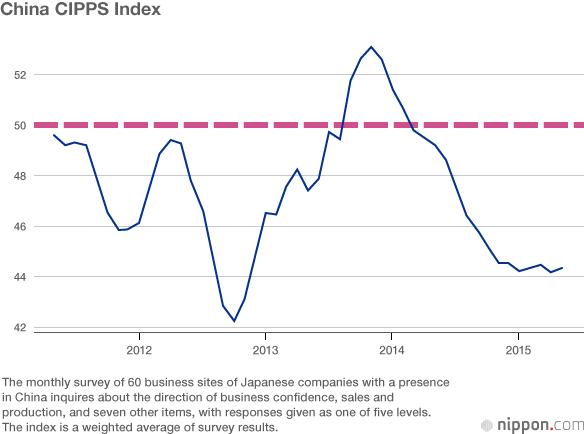

The Center for International Public Policy Studies engages in the fixed-point measurement of China’s economy based on its own research methods. In 2011 it began preparing the China CIPPS Index, derived from a monthly survey of business sites of Japanese companies with a presence in China. Around early 2014, this led to the composition of the China CIPPS Index in its current form, with data from 60 respondents.

According to this index, China’s economy has steadily worsened since the start of 2014. Stock prices in China, however, continued climbing from the latter half of that year, reaching very high levels before collapsing in June 2015. Stock prices plunged once again on the Shanghai Stock Exchange in January 2016, and the sudden implementation and then withdrawal of a circuit breaker generated enormous turmoil. The Chinese yuan weakened, and major concerns about the direction of the Chinese economy spread around the world.

The phenomenon to observe here is the extreme gap between the real economy, indicated by the China CIPPS Index, and stock-price trends. As if trailing the index, stock prices have fallen sharply since mid-June 2015. With the collapse of the stock-market bubble, the Chinese economy is looking quite different from what it was before, and financial distress has become serious in production and sales operations.

Capital Flows Out of China

What explains the developments that followed the collapse of the stock-market bubble? One factor is the sustained outflow of funds from the domestic economy into foreign markets. Prior to the collapse of the bubble, Chinese people likely had little inkling of how serious things would become both for themselves and for the country as a whole. Indeed, developing such foresight may be difficult in China, where the market’s price discovery mechanism is disregarded and the price signal plays little part in the allocation of resources.

Now that stock prices have collapsed, however, there is little chance that a new investment mechanism will take hold in the domestic economy. The vanishing of attractive domestic investments is accelerating the outflow of funds into foreign markets, and foreign economies are choosing to avoid China as a target for direct investments. As a result, investments have stalled, and productivity can no longer be expected to grow through higher investments. In the future, financial distress will likely give rise to further bad debts. These developments occurring in succession will without question turn the growth rate in an adverse direction.

The outflow of funds following the collapse of the stock-market bubble gave rise to the view that the yuan would continue to depreciate if left up to the market. The yuan has in fact depreciated sharply since autumn 2015. Instances when the Chinese monetary authorities will need to intervene in foreign exchange markets to sell dollars for yuan can be expected to increase. China’s foreign exchange statistics since August 2015 clearly reveal this situation. Selling dollars to buy yuan means that yuan funds that should have remained in the domestic private sector are absorbed into the foreign exchange account, thereby creating a counterflow to monetary easing. To ensure that funds will continue to flow into the financial sector as a whole, monetary authorities will be compelled to adopt such measures as further reduction of the reserve ratio, the amount of cash that banks must hold in reserve.

China is currently making such emergency monetary responses. The fact that the Chinese authorities are unable to guide the value of the yuan lower so as to increase the export of Chinese products and work off excess domestic inventories signifies that the outflow of funds has already begun. Thus, the possibility should be entertained that the growth of the Chinese economy has reached a major turning point.

Even Pensioners Flock to Stocks

Despite the possibility that the cash positions of Chinese companies had deteriorated sharply in 2015, stock prices continued to rise. This phenomenon is a tricky one to explain.

In July 2015 I had the opportunity to talk with the president of a company involved in automobile sales. Stock prices had already taken a dive in June. He told me that since it had become extremely difficult to sell automobiles, he would have to grin and bear it for a while. Businesses experiencing cash flow problems were no longer in a position to buy commercial vehicles. I asked him about stock prices. Why did stocks continue to surge in 2015 while companies were encountering cash flow problems? If cash positions had worsened for industry as a whole, surely stocks should not have risen so high. His reply to this question was extremely interesting.

Since cash positions had worsened for China’s economy as a whole, sales of built-for-sale homes were certain to slump, prolonging the sluggishness in housing prices. This situation would be hard to accept for people trying but unable to join the petite bourgeoisie. Interest on deposits had already been greatly reduced, and interest income could no longer be counted on to match the rate of inflation. These people were looking for a place to invest their financial assets, and small-lot stock investments became an outlet for them. Somewhat earlier, bonds with relatively high yields could be bought through the shadow banking system, but this possibility had now been blocked with the reform of regional public finances. At that time, the only place to realize financial gains was the stock market.

The wealthy were not being lured by the rise in stock prices, though. So who were these Chinese buying stocks? The president of the auto dealer told me that it was ordinary folk, and even pensioners, who were investing in the stock market. Low-income people were speculating in stocks with funds that should have been used for living expenses.

State-Owned Companies’ Fund-Raising Launched Stock-Market Boom

In the first half of 2015 Shanghai stunningly placed second after Hong Kong in a global ranking of funds raised through initial public offerings. In 2014 Shanghai had ranked eleventh.

A characteristic of IPOs in Hong Kong is that China’s state-owned companies account for an extremely large share. This indicates that state-owned companies have been raising funds to deleverage, that is to say, to reduce their debt loads. Furthermore, more often than not, it was small-scale investors who invested these funds. China has continued to release statistics that do not reflect economic reality. In the background, distortions have likely been appearing in wealth formation that may have been widening class differences.

The Gini coefficient is one means of measuring income inequality. The coefficient released by the Chinese government reveals that income differences have progressed to the point where it would not be surprising if social unrest broke out. The dramatic fluctuations of stock prices may have exacerbated disparities not just in income but in asset holdings as well.

Excess Investments, Productive Capacity, and Resource Consumption

During China’s high-growth period, investments disregarded an enterprise’s future prospects and were made without forethought as ends in themselves. As a result, such material industries as iron and steel, nonferrous metals, and petrochemicals are burdened with excess investments and excess productive capacity. China has become a high-resource-consumption economy.

China’s iron and steel production accounts for half of global production, and overcapacity is becoming an issue. Capacity for crude steel production is likely in excess by nearly 400 million tons. Judging from data for the first half of 2015, China’s export of steel materials can be estimated to be easily more than 100 million tons, even though the turmoil of international commodity prices actually worsened in the second half of 2015. China’s production of crude steel for export corresponds to total production in Japan, another major producer, contributing to sharp worldwide falls in steel prices. And petrochemical products can be expected to face an equally serious situation.

China is the world’s second largest economy. Now that its current situation has become apparent, its economy and economic management are being viewed with skepticism around the world.

Backdrop to Muddled Monetary Policy

Giving a coherent explanation of China’s recent economic management policy is no easy matter. Here we analyze the fluctuation of economic policy in terms of three policy targets that were unlikely to be achieved simultaneously. Our analysis examines China’s economy according to three periods: (1) from 2014 to June 2015, (2) from June to November 2015, and (3) the period since November 2015.

In period 1, monetary policy focused on the reduction of corporate debt as deleveraging became an issue for China’s economy as a whole. In period 2, as stock prices plunged, arbitrary interventionist measures were repeated, and multiple emergency responses were adopted to prevent China being “sold off” through the sale of yuan in foreign exchange markets. In period 3, China’s policy stance underwent a change after the yuan was added to the International Monetary Fund’s currency basket for special drawing rights, epitomizing the internationalization of the Chinese currency.

Monetary policy during period 1 can be described as one intended to support stock prices as cash positions worsened in the corporate sector and as prospects grew for an inflection of the economic growth rate. Despite the urgency of easing monetary policy, fears of the net outflow of funds from China caused monetary authorities to sell dollars for yuan so as to maintain the yuan’s value, an intervention that was pursued in earnest from the summer of 2014 onward. Since this intervention would absorb yuan from the funding market, the reserve ratio had to be reduced multiple times.

Initial public offerings by the corporate sector were promoted by trumpeting the effect that such sham monetary easing has in supporting stock prices. The funds of individual investors flowed into the stock market, and companies raising funds through the stock market were able to pay off their debts. At first glance, it would appear that this policy achieved its objective.

In period 2, as the prices of stocks collapsed, measures were implemented arbitrarily to impede their sale. While the regulation of capital transactions was viewed as a matter of course, the sharp decline of the yuan had to be avoided, and intervention to sell dollars for yuan continued. An unstable monetary situation remained in place.

In period 3, with the yuan being added to the SDR currency basket, the immediate objective of internationalizing the yuan was achieved. From about this time, a policy of leaving the value of the yuan up to the market began to take shape. It was from November 2015 to the end of the year when Chinese with an interest in economic policy began asking me how far I thought the yuan might fall.

The sale of the yuan from the start of 2016 and the ensuing decline of stock prices could not be arrested. The repetition of arbitrary intervention is likely interfering with market players’ ability to analyze which interventions are causing which effects and at which point adverse secondary effects materialize.

Murky Conditions in China

Prior to the sharp decline of Shanghai stock prices in June 2015, there were only two sources of information from China that influenced global markets. The first was the monthly Caixin/Markit Purchasing Managers’ Index, and the second was speculative information about government intentions to devalue the yuan.

The former can be likened to being lost in a pitch-black space with only a feeble lamp in hand illuminating the area around one’s feet. Whether a huge abyss lies ahead is concealed in the dark. There is, however, no other indicator available to illuminate where one is standing.

The latter stems from the impossibility of making any sense at all of the aims of the Chinese economic authorities. Although it should be clear that the devaluation of the yuan does not offer a solution for the Chinese economy, market players cannot help speculating that the Chinese authorities might actually be contemplating such a move.

The impenetrable fog shrouding the Chinese economy and government policies has led to the rapid destabilization of world resource prices. This was the situation from December 2015 to February 2016. Market players are now wondering whether the G7 summit in May 2016 can come up with measures that would reverse investors’ flight from risk.

(Banner photo: World stock prices continue to plummet due to uncertainties about China’s economy and resource prices. © Jiji Press.)foreign exchange stock prices Chinese economy resource-consumption- driven economy Center for International Public Policy Studies (CIPPS) collapse of speculative bubble iron and steel plunging stock prices