Are Pay Hikes the Way to Revive Japan’s Economy?

Politics Economy Society- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Spring Wage Hikes of Two Percent Plus

The 2014 shuntō spring labor offensive, as labor unions call the negotiations with management that take place every spring, drew to an end in March as corporations presented their responses to union demands for wage increases. According to a survey of the results of labor-management negotiations at major companies released by Keidanren (Japan Business Federation) on April 16, 2014, the settlements resulted in an average increase of 2.39% in monthly wages for the new business year starting in April. Although this figure also includes regular annual seniority-based wage hikes, we can assume that base salaries went up roughly 0.51%, given that wage increases in 2013 (when base pay was not hiked) averaged 1.88%.

The Keidanren survey, however, covers only a small number of major companies. For a more complete picture, we must await the Ministry of Health, Labor, and Welfare’s statistics on shuntō wage demands and settlements among major private enterprises. As for currently available data, there is the pre-shuntō outlook on wage increases compiled by the Institute of Labor Administration, which predicted a 2.07% rise this year. As past predictions in this survey have largely been on the mark, it appears safe to say that wages rose by 2.0% or more overall.

“Base-Up” and Regular Wage Hikes Explained

In Japanese, this hiking of base pay is known as bēsu appu (“base-up”), or bea for short. The idea of the “base-up” is common knowledge among those who started working at Japanese companies before 1990. But after the bursting of the economic bubble at the start of the 1990s, employers abandoned this practice, and it remained out of general use for many years. So a brief explanation of the concept, along with that of regular wage hikes, is probably in order.

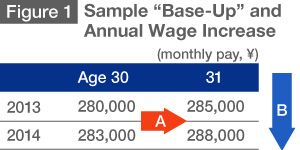

A base-up is not simply an across-the-board increase in wages. It specifically refers to a hike in the base pay, the core portion of the salary. Meanwhile, Japanese companies conventionally apply a seniority-based compensation system under which wages rise with each year of continued service. This regular annual hike is what is called teiki shōkyū, literally meaning “periodic wage increase.” Figure 1 illustrates the two forms of pay hikes using hypothetical figures with age as a surrogate for years of service .

The ¥5,000 difference between the salaries of a 30-year-old and a 31-year-old (arrow A) represents the regular annual wage hike based on seniority. Meanwhile, the ¥3,000 increase in 2014 for both ages (arrow B) corresponds to the base-up.

The ¥5,000 difference between the salaries of a 30-year-old and a 31-year-old (arrow A) represents the regular annual wage hike based on seniority. Meanwhile, the ¥3,000 increase in 2014 for both ages (arrow B) corresponds to the base-up.

While both the base-up and regular wage hikes mean higher labor costs, businesses are particularly averse to the former. So long as they keep to just the regular annual hikes, neither the total amount of wages nor the average wage will change over time if they recruit a constant number of new employees every year, with older employees leaving at a steady pace as they reach the mandatory retirement age. (Naturally, average wages will decrease if a company takes on a bigger group of recruits every year and increase if the group gets smaller.)

In contrast, raises in base pay will elevate average wages and thus push up the total amount of wages paid. Since the bubble’s collapse, Japanese businesses have struggled to cope with sharp rises in the value of the yen and declines in demand. While they have been willing to reward their employees with bonuses at times of high profits, they have gone out of their way to avoid base-ups, which spell higher fixed expenses that could strain corporate finances. Hence the recent newspaper headlines about the first base pay raises in two decades.

Wage Hikes Driven by Necessity

The Kantei (the prime minister’s office) played a visible part in pushing for the latest round of base-ups. This was due to mounting criticism from the media and opposition parties regarding the administration’s drive to induce mild inflation. By way of background, when the Liberal Democratic Party returned to power and Abe Shinzō became prime minister for the second time in December 2012 (having previously held the post from 2006 to 2007), the first “arrow” of his economic program was bold monetary relaxation to overcome deflation and get the economy back on track. This led to the adoption of a 2% inflation target. But higher prices without higher wages would only make life harder for the people, critics said.

In response, the administration set up the Government-Labor-Management Meeting for Realizing a Positive Cycle of the Economy. In this forum, where government officials were joined by representatives from business and labor, the government asked that profits gained from the correction of the overvalued yen and recovery of the economy be translated into higher wages. This met with the criticism that it is not proper for the government to poke its nose into decisions about wages, which ought to be left up to labor and management. (I agree.) But the recent base pay hikes did not necessarily come about in response to this government initiative. Improved economic conditions have gradually led to labor shortages in fields with relatively poor working conditions, forcing employers to offer higher pay. Besides, it is wishful thinking to assume that corporations would raise wages at the beck and call of the government. I suspect that companies are just saying they cooperated with the government when in truth they hiked their wages out of necessity.

Wages had been stagnating for years because more people were taking up non-regular jobs, while the number of those in regular employment remained constant. From businesses’ point of view, once employed, regular workers are difficult to fire when the economy sours. So even if demand increases in the short term, they prefer to hire non-regular workers if they are not confident that the upward trend will persist.

Because wages are lower for non-regular employees, higher ratios of non-regular to regular workers translate to lower average pay. Of course there is also the big issue of non-regular employees receiving smaller paychecks even when they are doing the same work as regular employees, but part of the reason for this is that non-regulars put in fewer hours each month than their regular counterparts. What we should really be looking at is wages per hour. And in order to determine whether wages are actually rising under Abenomics, as Abe’s economic program has been dubbed, we need to look at how hourly pay is changing.

There are no official statistics on this indicator in Japan, but the Ministry of Health, Labor, and Welfare’s Monthly Labor Survey tracks data on total cash earnings per month and total hours worked, both of which include overtime. Dividing total cash earnings by total hours worked will yield hourly pay. Total cash earnings also include bonuses, however, so figures are higher for those months when bonus payments are made. Seasonally adjusted data that take such fluctuations into account should provide a good picture of monthly trends in wages per hour.

Work Hours on the Rise under Abenomics

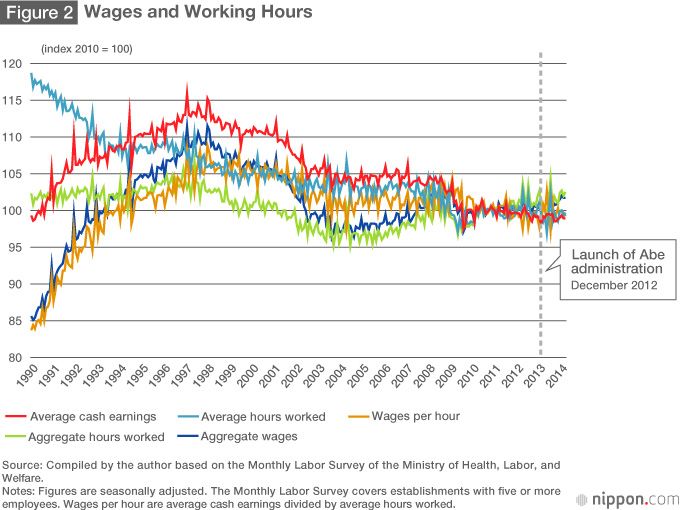

Figure 2 shows changes in average cash earnings per employee, average hours worked per employee, wages per hour, aggregate hours worked, and aggregate wages from 1990 onward (expressed in index numbers, with 2010 as the base year). Aggregate hours worked are calculated by multiplying the total number of employees by average hours worked, thus giving the total number of hours worked by all employees. And aggregate wages are calculated by multiplying aggregate hours worked by wages per hour, thus giving the total amount of wages earned by all employees.

If we look at the period since December 2012, when Abe became prime minister, we find that cash earnings, hours worked, and wages per hour have been fluctuating too greatly from month to month to tell whether they are trending upward or downward. But aggregate hours worked and aggregate wages have been on the rise since that month. In other words, although wage rates were not rising during the course of 2013, the grand total of wages paid was growing, reflecting the rise in the number of people employed under Abenomics. And if total wages have genuinely been increasing, people should be feeling better off.

Not much more can be said until additional data becomes available over time. But the wage hikes implemented at the start of the new business year in April 2014 should mean an increase in the figures for hourly wages.

Impractical Wage Hikes Slow the Economy

A longer-term look at these statistics reveals more intriguing facts. Going all the way back to 1990 in figure 2, we see that average cash earnings rose form 1990 to 1997, while average hours worked declined. It goes without saying that wages per hour, as the quotient of cash earnings divided by hours worked, climbed faster than cash earnings. Wages per hour and aggregate wages advanced 23% and 25%, respectively, from 1990 to 1998, despite the fact that the economy suffered repeated dips and nominal gross domestic product grew by only 15% over the same period. If wages go up while the economy is in the doldrums, it is only to be expected that profits will contract and capital investment will drop, further slowing the economy. This is part of what caused the Japanese economy to stagnate from the 1990s onward.

Wages subsequently fell, stabilizing from around 2002 on, after the excessively high rates had been corrected. With this the Japanese economy recuperated and came to enjoy annual growth of about 2%, before being thrown back into the doldrums by the global slump following the collapse of Lehman Brothers in 2008. It is now in the process of recovering under Abenomics.

These observations suggest that wage hikes out of touch with economic reality have the effect of setting back the economy. In other words, attempts to improve the economy by forcing wages to go up may perversely cause economic conditions to deteriorate. Wages rose even during the administration of Koizumi Jun’ichirō (2001–6), when people complained that economic growth was failing to produce perceptible improvement in ordinary citizens’ lives. To sustain the current Abenomics-driven economic recovery, it would be wiser to wait for lower unemployment rates brought on by near-term recovery to induce pay hikes accompanying the resulting labor shortages.

(Originally published in Japanese on April 23, 2014. Title photo by Jiji Press.)

Abenomics Kantei Base-up shuntō spring labor offensive Lehman Brothers bankruptcy lifetime employment wage salary