Rebuilding Japanese Finances: Tackling a ¥1 Quadrillion Debt

Politics Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Japan’s Debt Rating Takes a Hit

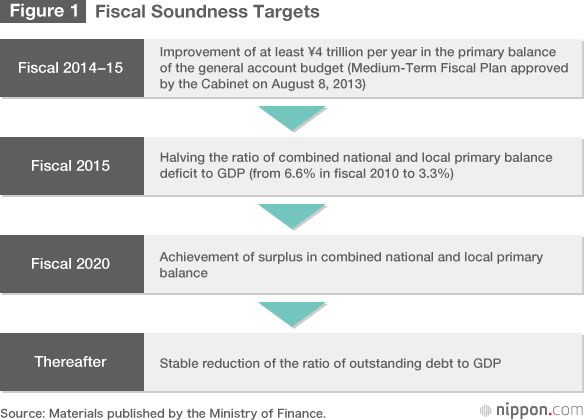

In mid-November 2014, Prime Minister Abe Shinzō announced he would dissolve the House of Representatives and call a general election in the following month. At the same time, he decided to delay the next hike in the consumption tax (from 8% to 10%), which had been scheduled for October 2015, and to adhere strictly to “fiscal soundness targets” that seek to restore the primary balance(*1) of the government budget to the black by fiscal 2020. Economists and other experts are generally of the opinion that achieving the fiscal soundness targets by the deadline will be an extraordinarily difficult feat.

Reacting to the delay in the next consumption tax increase, the US rating agency Moody’s Investors Service downgraded Japanese government bonds by one notch, from Aa3 to A1, on December 1. Moody’s cited increasing uncertainty about whether Japan could achieve its budget deficit reduction targets. A1, the fifth highest of 21 ranks used by the company, is below the ratings assigned to China and South Korea, placing Japan on a par with Israel, the Czech Republic, and Oman.

The OECD’s Worst Debt Balance

According to the Ministry of Finance, the national debt, calculated as the total balance of government bonds and borrowings, stood at ¥1.04 quadrillion as of the end of September 2014. Divided by the population of Japan on October 1 (some 127 million), this figure translates to borrowings of roughly ¥8.17 million per person. The debt balance is forecast to increase to ¥1.14 quadrillion by the end of March 2015.

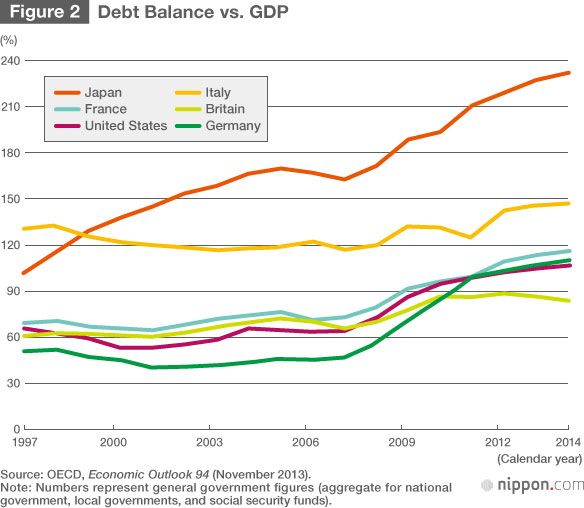

Japan stands head and shoulders above everyone else in international comparison of government debt versus GDP, according to the Organization for Economic Cooperation and Development. In 2014, Japan’s balance of government debt was 231.9% of GDP, more than double the level for France, Britain, or the United States. Japan finds itself at a more precarious level than Greece, a country that has sparked an economic crisis in Europe due to its worsening fiscal conditions.

The Burden of a Graying Population

Japan has a chronic shortage of revenue against spending. The nation covers the gap by borrowing money, generally in the form of government bond issuance. This is the primary factor behind the burgeoning budget deficit. The solution, though, is not as easy as simply increasing revenue and slashing expenditures. Indeed, there are many spending items that will only continue to increase.

Among the most prominent outlays are pension, healthcare, and nursing care insurance benefits paid to the elderly. Combined, they account for roughly three-quarters of social-security-related spending, which itself accounts for 31.8% of total expenditures (¥95.9 trillion) in the fiscal 2014 budget. These numbers highlight how difficult it will be to restrain this spending as the population ages.

We should note that debt servicing accounts for roughly one-quarter (24.3%) of total expenditures for fiscal 2014. In other words, servicing Japan’s debt and maintaining its social security systems account for more than half of the overall budget. This is a major factor behind the “fiscal rigidity” seen in Japan. Indeed, this rigidity has been an issue for Japan ever since the balance of government debt began expanding in the late 1960s.

JGB Yields to Plummet?

Japan can no longer procrastinate in rebuilding its finances. Fiscal soundness will only become more difficult to achieve as society grows grayer—unless appropriate funding is provided for social security. In June 2012, when the Democratic Party of Japan controlled the government, there was an agreement among the three major parties—the Liberal Democratic Party, Kōmeitō, and the DPJ—to stabilize social security funding with an integrated package of reforms to both social security and the tax system. Subsequent legislation hiked the consumption tax in April 2014 as part of measures to secure the needed fiscal base.

It is by no means certain that Japan will be able to achieve its fiscal soundness targets by the time the Tokyo Olympics are held in 2020. The question for the markets is whether Japan has the will and ability to do so at all. As Japanese government bonds become riskier, investors could lose confidence in them, triggering a sharp decline in their price (which is equivalent to a sharp increase in interest rates).

There is no magic pill for solving fiscal problems. The government must maintain discipline and move steadily toward a sound fiscal footing. What this specifically means is that it must use the breathing space gained by delaying the next consumption tax hike to ensure that the economy moves out of deflation onto a growth trajectory and to achieve palpable savings through reforms to the social security system and the nation’s fiscal and administrative structures.

The Need for Clear Leadership

The balance of long-term government debt is far too large to be reduced simply by increasing the consumption tax, though. Economists argue forcefully that the government alone, through spending cuts and tax increases, cannot achieve this goal; solid economic growth is a must to reduce Japanese borrowing. Along with the necessary work of eliminating budgetary waste, Japan must also fuel an economic recovery to boost tax revenues. Here the spotlight shines on the “three arrows” of Abenomics, which aim to bring about this state of affairs.

The December 2014 House of Representatives election gave the LDP-Kōmeitō coalition four years to run the government. While campaigning, Prime Minister Abe argued again and again that “the only path forward is economic recovery” through Abenomics. Having secured a rock-solid political foundation, the government must now turn its attention to the painful systemic and structural reforms that will translate into primary balance surpluses.

(Banner photo: The Ministry of Finance. © Jiji.)

(*1) ^ Primary balance (PB): The balance between revenues (tax and nontax) and expenditures (other than debt servicing, or repayment of principal and payment of interest on government bonds). The primary balance is an indicator of the government’s ability to cover its policy spending with tax revenue at a given point in time. In Japan, it has been in the red since the early 1990s, and the government considers bringing it into the black a milestone on the road to fiscal soundness.

Abe Shinzō deficits primary balance Abenomics fiscal policy government bonds fiscal soundness targets fiscal rebuilding social security spending