The Uncertain Future of Japan’s Machine Tools Industry

Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

“To live well, a country must produce well.” These words of wisdom come from the introduction to Made in America: Regaining the Productive Edge, published in 1989 by the Commission on Industrial Productivity at the Massachusetts Institute of Technology.(*1) Prompted by concerns about the declining strength of American industry, the report aimed to sound a warning based on an analysis of burgeoning production in Japan and Europe in eight key industries—from the automotive industry to chemicals, civil aeronautics, electronics, and machine tools. The study concluded that a healthy industrial sector is vital to national strength. In the two decades since then, industrial strength has passed steadily from the United States to Japan. In the near future, it looks likely to pass from Japan to the newly emergent economies of China and India.

There is a close correlation between the growth of the machine tools industry and a country’s economic growth rate. Not surprisingly, therefore, demand for machine tools is currently surging in China (population 1.3 billion) and India (population 1.1 billion). The volume of demand in these countries is on a different level of magnitude. Chinese firms contracted to provide electronic manufacturing services for components used in smart phones and tablet devices such as Apple’s iPhone and iPad have introduced machining centers that can process more than 2,000 units at once. Taiwanese and Korean companies are also competing aggressively to provide low-cost machine tools to the China market. In China, as well as in India and the Asian market in general, manufacturers from China, Taiwan, and Korea are using competitive strategies and rapidly catching up with Japanese and German firms. Where does this leave the Japanese machine tools industry? Do Japanese firms now face the same fate that befell their American counterparts? Is the Japanese machine tools industry destined for inevitable decline?

Japan’s 27 Years at the Top

Machine tools are often referred to as “mother machines.” They are essential parts of the manufacturing process for everything from cars, planes, and trains to everyday objects like mobile phones, cameras, and clocks. Truly these are the “machines that make machines.”

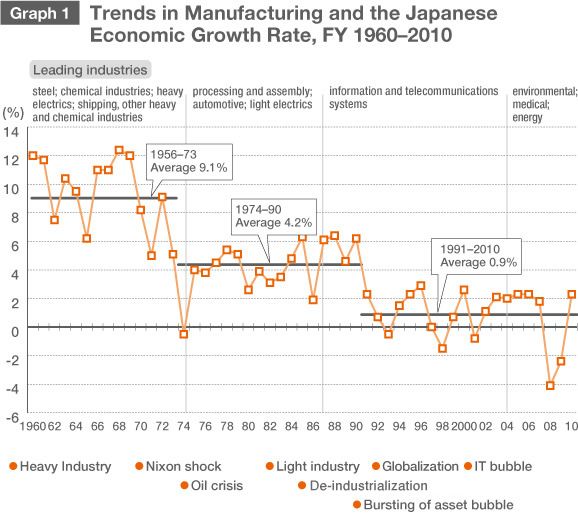

As mentioned above, the growth of the machine tools industry is closely related to a country’s economic growth rate. In this context, it is instructional to take a look at the overall trends for GDP and key industries in Japan since the end of World War II (Graph 1). During the period of rapid economic growth from 1956 to 1973, when the average annual growth rate was 9.1%, the Japanese economy was primarily driven by swift growth in heavy industry and chemicals, namely: steel, chemicals, heavy electric equipments, and shipbuilding. These were necessary to power the rebuilding of the economy ten years on from the end of the war.

In the subsequent period, from 1974 to 1990, when annual growth averaged 4.2%, the focus switched to automobiles, light electrical appliances, and the processing and assembly industries, as Japan became the workshop of the world. The Japanese economy and its industries have continued to mature since then, and today the trend is toward industries related to the environment and medical care. Meanwhile, the BRIC countries (Brazil, Russia, India, and China) are shifting from heavy and chemical industries to processing and assembly.

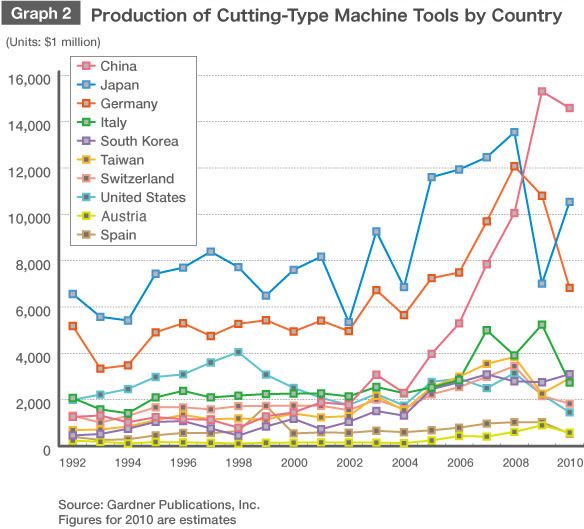

Graph 2 shows changes in cutting machine tool production figures for major countries. (Information taken from a survey conducted by Gardner Publications, Inc., USA.) The total value of production for 2010 (28 countries) was approximately $48.23 billion. Of this, Japan was the second largest producer ($10.54 billion, 22%), behind China ($14.59 billion, 30.2%). Germany ($6.83 billion, 14.2%) was third. These three countries, collectively, have dominated the market in recent years. Japan overtook the United States as the world’s leading producer of machine tools in 1982, having boosted its national strength through the mass production of automobiles. Japan remained number one for 27 years, until 2009.

American and European Firms in the 1970s

Back in the 1970s, the United States was home to many outstanding machine tools manufacturers, such as Cincinnati Milacron, Moore, Warner & Swasey, Burgmaster, Giddings & Lewis, and Kearney & Trecker. When I covered the National Machine Tool Exposition in Chicago (one of the three major international machine tools trade fairs) as a rookie reporter in the early 1970s, I visited several of these leading companies myself. As a place that produces strategic components for aircraft and automobile manufacturers, a machine tools factory would normally be off-limits to outsiders. But people seemed willing to go out of their way to help me when they heard I had traveled all the way from Japan.

At the time, Americans took great pride in their country’s technology, and were extremely welcoming to visitors. Technicians from Japanese machine tools manufacturers all aimed to emulate the United States. The K&T Toshiba Machine joint venture established in Japan by Toshiba Machine Group, the prototype for today’s machining centers, was also inspired by an urge to match American companies.

American journalist Max Holland, the son of a former Burgmaster employee, wrote the following in the introduction to When the Machine Stopped, his 1989 study of the Burgmaster company: “Once, manufacturing and the U.S. economy were almost synonymous. The American system of manufacturing, or mass production, was the chief emblem of an economy that was both the wonder and envy of the world.”(*2) In the 1970s, American machine tools companies were an absolutely integral part of the American system. Nevertheless, one after another these companies vanished from the scene, as did Burgmaster itself, as described by Holland in his study. Machine Tool Scoreboard, published in March 2011 (Gardner Publications, Inc.), ranks the world’s top 143 companies in 2010 according to production volume. Fifteenth-placed Gleason, a maker of grinding tools for car gears, was the only American survivor on a list once dominated by American firms.

Europe too had its share of successful manufacturers. European craftsmanship was a byword for precision and quality, and Japanese manufacturers fell over themselves to enter technical cooperation agreements with European firms in the 1960s and 1970s. As in the United States, however, firms that had been market leaders failed to keep up with the changing times and were subject to takeover or sale. Although the names survived as brands in some cases, in reality most of these firms ceased to exist as independent entities. Among those who fell by the wayside were leading firms such as Sip and DIXI (both jig borers, Switzerland), Hauser (jig milling cutters, Switzerland), Reishauer (gear-grinding machines, Switzerland), Cazeneuve (copying lathes, France), and Jones & Shipman (grinding machines, United Kingdom). In spite of this decline, 18 German firms were listed in the Machine Tool Scoreboard, including Trumpf (2nd place), Gildemeister (5th), Maag (12th), Schuler (14th), and Index (17th). Germany continues to be Japan’s strongest competitor in today’s machine tools industry.

Japanese and German Dominance Challenged by China

It was during the early 1980s that Japan came to the fore. Japan was the first to successfully implement numeric control into its machine tools, and this breakthrough soon enabled it to overtake European and American firms still wedded to the idea of producing high-end, multi-function machines. FANUC, a manufacturer of computer numerical control devices and robots, also made a major contribution to placing Japanese manufacturers on the big stage internationally.

In the August 2011 edition of Machine Tool Scoreboard, 6 of the top 10 companies are Japanese: Yamazaki Mazak (1st place), JTEKT (4th), Komatsu (7th), Mori Seiki (8th), Amada (9th), and Okuma (10th). Overall, 37 of the 143 companies ranked in the tables are Japanese (26% of the total). Japan is followed by Germany, with 18 companies (13%). These two are far ahead of the rest. China still has only six companies in the list (4.2%). But in terms of production, China’s machine tools industry is worth over $4 billion more than Japan’s. Given the size of China’s population (10 times greater than Japan’s), and its rapidly expanding infrastructure (water, sewage, electricity, gas, rail networks), it is obvious that China’s huge market far outstrips the already mature Japanese market. Barring any major unexpected events, China is almost certain to become world leader in machine tools production in the near future.

Japanese machine tools are particularly strong in the fields of high-precision, composite processing, and machining of hard-to-cut materials. They offer unrivalled levels of precision, timeliness, and price, honed in the fields that helped make “Made in Japan” as a byword for safety and reliability—including tools used in the automotive industry (Toyota) and the electronics industry (Panasonic, Hitachi, and Sony).

Japan’s machine tools manufacturers may no longer be able to match China in terms of production value, but Japanese firms are still comfortably ahead in terms of high quality, processing of difficult-to-cut materials, and composite processing technology. Examples include the carbon fiber reinforced plastics used in the wings, fuselage, and wing center box of the Boeing 787 and Airbus 350, which make up 50% of the total weight of the aircraft, as well as titanium and high-hardness materials. But the difference in scale between the Japanese and Chinese machine tools markets will only continue to grow in the years to come. Sooner or later, the quality of Chinese machine tools will improve, and in time the Chinese can be expected to encroach, in terms of both quality and quantity, on the areas where Japanese-made machine tools currently hold an advantage. The decline of American manufacturers was not due solely to the rise of Japanese firms. They were also weakened by the storm of mergers and acquisitions that followed the chaos of consolidation in the 1960s and 1970s. It is hard to avoid the thought that the same fate may be lying in wait for Japanese firms.

The Importance of the Automotive Industry

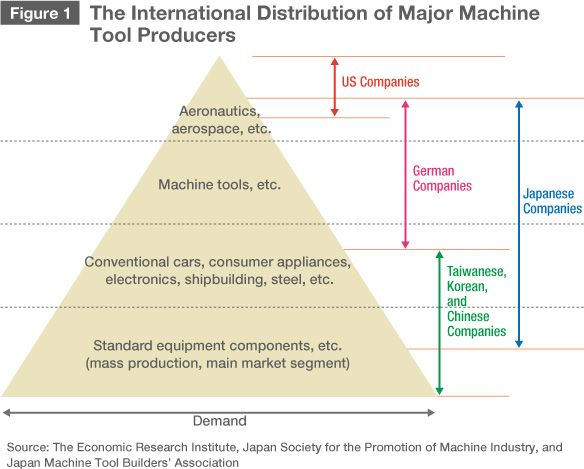

Figure 1 shows the distribution of the international machine tools market (based on materials provided by the Economic Research Institute, Japan Society for the Promotion of Machine Industry, and Japan Machine Tool Builders’ Association). The Japanese machine tools industry covers a wide range, including everything from space and aeronautics to regular consumer goods. In terms of volume, however, it has been said that the machine tools industry relies heavily on the automotive components industry, which produces between 20,000 and 30,000 separate components and accounts for 60% of all machine-tool orders.

Japan has 12 automotive manufacturers, including Toyota, Nissan, Suzuki, and Honda. Between them, the companies produced some 9.63 million cars in 2010 (a 21.3% increase from the previous year). Components makers (Tier 1 and Tier 2) supply parts to these manufacturers. The Japan Auto Parts Industries Association has 442 members, including companies such as Denso, Aisin Seiki, NTN, and KYB. Further down the pyramid is a wide base of Tier 3 and Tier 4 companies that are not members of the association. Total capital investment in the automotive industry (scheduled investment for fiscal 2008) was worth ¥1.62 trillion, equivalent to 21.6% of the total manufacturing industry (¥7.52 trillion). Investment in machine tools makes up just a small fraction of this total. According to statistics compiled by the Japan Machine Tool Builders’ Association, orders for the automotive industry were worth ¥89.37 billion in 2010, 9.1% of the total.

On the surface, this may not seem to represent a 60% dependence on the automotive industry. But when orders for components and equipment for general purpose machinery, electrics, and precision machinery destined for the automotive industry are all included, the industry does indeed make up roughly 60% of all orders. The consequences are clear: the Japanese manufacturing industry as a whole is structured in such a way that it is certain to stagnate if an economic downturn affects the automotive industry.

This is both the strength and weakness of the Japanese machine tools industry. At the moment the automotive industry is moving away from Japan and increasing production in factories overseas. If the governments of these countries decide to encourage the development of their own automotive industries and try to freeze out Japanese products by introducing legislation favoring locally produced components or machine tools, Japanese machine tools manufacturers will find themselves without a leg to stand on.

Japan’s Sturdy Machine Tools Manufacturers

Around 200 companies in Japan produce machine tools, including 77 of the 92 members of the Japan Machine Tool Builders’ Association, and 27 of the 37 members of the Japan Bench Machine Tool Builders’ Association. Together with companies that are not members of either organization, these firms make up the Japanese machine tools industry. The pioneer in terms of overseas production was Yamazaki Mazak, which established a factory in the United States in 1974. The current state of Japanese overseas production in 2011 is shown in Figure 2. Companies have expanded production overseas in a variety of ways. Some produce computer numerical control machine tools in factories in the United States, Singapore, or Taiwan for export to Japan, the United States, Europe, China, and Southeast Asia. Examples of this approach include Yamazaki Mazak, Makino Milling Machine, Takizawa Machine Tool, and Sodick. Other companies have formed joint ventures with European manufacturers. Mori Seiki, for example, started production in the China factory belonging to Gildemeister, a German firm. Takamatsu Machinery has linked up with a Taiwanese company to establish a production base in China. These firms are using Japan’s advanced technology to try to develop main market segments overseas.

Other companies compartmentalize their business, producing high-quality machine tools and high-precision machine tool components in Japan and manufacturing mass-produced bulk machines overseas. If they can continue to display the same resilience and flexibility, Japanese machine tools manufacturers may avoid repeating the mistakes of American companies.

Figure 2. Overseas Production by Japanese Machine Tools Manufacturers

| United States | Citizen Machinery, Yamazaki Mazak |

| Brazil | JTEKT |

| United Kingdom | Yamazaki Mazak |

| France | Mori Seiki |

| Switzerland | Mori Seiki |

| South Korea | FANUC, Nishida Machine |

| Taiwan | Okuma, Takisawa Machine Tool |

| China | Brother Industries, Citizen Machinery, FANUC, Hakusan Kiko, JTEKT, Kiwa Machinery, Komatsu NTC, Koyo Machine Industries, Makino Milling Machine, Mitsubishi Electric, Okuma, Shin Nippon Koki, Sodick, Takamatsu Machinery, Tsugami, Yamazaki Mazak |

| Philippines | Miyano |

| Thailand | Citizen Machinery, Enshu, Okamoto Machine Tool Works, Sodick |

| Singapore | Makino Milling Machine, Okamoto Machine Tool Works, Yamazaki Mazak |

| Vietnam | Citizen Machinery |

| India | FANUC, Makino Milling Machine |

Source: Japan Machine Tool Builders’ Association

Nevertheless, it is important to bear in mind the remarks made by Yoshino Hiroyuki, former president of Honda Motor Co., in his speech at the Japan International Machine Tool Fair in 2008. “In our newly operational factory in Thailand,” he said, “we have introduced to our engine processing line machine tools made in India and China that cost around 40% less than machines made in Japan. The results have been impressive. Japan needs to reconsider the question of cost.” In a rapidly changing era, it is difficult to predict how things will look in five years’ time. But companies that lack a distinctive individuality of their own, that do not have the necessary skilled personnel, and watch complacently as the world market changes around them, face tough times in the years ahead. Only with continued hard work and inventiveness can Japanese machine tools manufacturers hope to rise to the challenge.

The author visits another manufactureing company

The author visits another manufactureing company

United States China India Europe America Machine tools Taiwan Korea auto industry cars Hikosaka Masao