Getting Serious About Fiscal Reform: Beyond Smoke and Mirrors

Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

As Japan marks the seventieth year since its surrender in World War II, the nation’s public debt has already passed every historical milestone. As a percentage of GDP, it exceeds the 200% recorded on the eve of Japan’s defeat. Of course, a government debt twice the size of the economy does not necessarily portend national insolvency, but it certainly increases the probability of a fiscal crisis.

Cognizant of this danger, the Japanese government has pledged to rebuild its finances through a combination of tax and social security reforms. In 2010 it adopted two key reform targets: to cut the primary budget deficit (central and local government combined) as a share of GDP in half by fiscal 2015 and to post a primary surplus by fiscal 2020.

As a key step to achieving these goals, the government of Prime Minister Abe Shinzō raised the national consumption tax from 5% to 8% in April 2014, in accordance with a previously approved tax plan. The same plan called for a further hike, to 10%, in October 2015, but last November the government opted to postpone the second increase until April 2017, amid concerns over flagging economic growth.

Meanwhile, the fiscal 2015 draft budget that the cabinet approved on January 14 of this year calls for ¥96.3 trillion in spending, the highest figure ever. While trimming the local allocation tax grants distributed to prefectural governments by ¥600 billion, the government boosted social security spending by ¥1 trillion. Altogether, spending grew by ¥500 billion over fiscal 2014. What are the implications for fiscal reform?

The Government’s New Math

In a press conference on November 14, 2014, Minister of Finance Asō Tarō had warned that it would be difficult to achieve the target of halving the primary deficit ratio by fiscal 2015 if the government postponed plans to hike the consumption tax to 10%. His assessment was based on the Cabinet Office’s latest Economic and Fiscal Projections for Medium to Long Term Analysis (released on July 25, 2014), which projected a fiscal 2015 primary deficit of ¥16.1 trillion even with the tax increase. Since government needs to hold the deficit to within ¥16.9 trillion to meet its target, this left precious little room to maneuver.

Nonetheless, in his post–cabinet meeting press conference on January 13 (a day before the cabinet formally approved the fiscal 2015 budget plan), Asō assured the nation that the government was still on track to meet the fiscal 2015 reform target. Is it really possible to reduce the primary deficit ratio by half even while increasing spending and putting tax increases on hold?

The honest answer is, “We don’t know yet.” The outcome depends on Japan’s economic performance in fiscal 2015, which begins in April 2015. Because GDP estimates go through several revisions, the corrected data for fiscal 2015 will not be available until December 2016. (The final figure is not released until the publication of the Annual Report on National Accounts a year later.)

However, if we go by the official estimates, the government can claim to have compiled a budget that—at least on paper—achieves the goal of halving the primary deficit ratio from the fiscal 2010 level. Unfortunately, this feat hinges on a combination of fortuitous circumstances and cynical expedients, neither of which will help Japan achieve fiscal sustainability in the long run. To understand this better, we need to take a closer look at the Finance Ministry’s accounting.

Kicking the Can

One factor behind the government’s budgetary coup is the relatively small impact the tax-hike delay is projected to have on fiscal 2015 revenue, thanks to timing and accounting technicalities. If each percentage point of consumption tax levied yields ¥2.7 trillion in government revenue, then by a simple calculation, an increase of two percentage points (from 8% to 10%) should yield ¥5.4 trillion. But the government projects that the tax-hike postponement will cost the government only ¥1.5 trillion in tax revenue in fiscal 2015. Why such a large discrepancy?

First, because the tax increase was not scheduled to take effect until October 2015, the middle of the fiscal year, only half of it was applicable to fiscal 2015. That yields ¥2.7 trillion. Next, during the course of fiscal 2015, the businesses on which the tax was to be levied would have paid the government only about 73% of that ¥2.7 trillion, or about ¥2 trillion, owing to discrepancies between accounting periods and transitional provisions covering long-term contracts and other situations.

Of the remaining ¥2 trillion, ¥500 billion was slated to be transferred to the prefectural governments in the form of local allocation tax grants. Of course, that ¥500 billion would show up as revenue at the local level, but because of the time gap, only a small fraction of it would have been reported in fiscal 2015.

Thanks to these technicalities, the combined cost of the suspended tax increase to national and regional budgets is estimated at only about ¥1.5 trillion in fiscal 2015. But by the same token, there will be no escaping the full impact (¥5.4 trillion) in fiscal 2016 and beyond.

Smoke and Mirrors

More problematic is the second factor enabling the government to reach its target—namely, the use of various nontax receipts to inflate revenue. The fiscal 2015 draft budget offsets a portion of the ¥1.5 trillion in lost tax revenue with ¥600 billion in receipts from such sources as the sale of government shares in NTT (Nippon Telegraph and Telephone Corp., a former government monopoly), transfer of surpluses from a housing investment fund, and payments from the Bank of Japan.

Much of this ¥600 billion is highly questionable from an accounting standpoint. For example, when the government sells its NTT shares, it is disposing of assets, resulting in a net increase in liabilities (debt minus assets). In this sense, it would be more appropriate to lump proceeds from the sale of NTT holdings with funds raised from bond issues. The situation is comparable to that of a family that draws on its savings to cover living expenses when its income drops. If the family begins with net liabilities of ¥8 million (a ¥10 million home loan minus ¥2 million in savings) and uses ¥1 million of its savings to defray living expenses, it will end up with net liabilities of ¥9 million (¥10 million minus ¥1 million). Budgetary finessing of this sort merely passes on the burden to our children and grandchildren. I believe we need to discourage such accounting shenanigans by setting up an independent, politically neutral agency staffed by highly qualified experts to compile trustworthy long-term budget forecasts and generational accounts for public release.

The third way in which the government has managed to reach its interim goal is by the legitimate means of reviewing public spending to hold down growth of the general account budget. Through this process, the government wisely trimmed about ¥1 trillion from initial projections to help offset the revenue lost through postponement of the consumption tax hike. Specifically, it saved about ¥500 billion (¥400 billion at the national level and ¥100 billion locally) by canceling enhancements to social security linked to the tax increase, and another ¥500 billion by prioritizing and streamlining public spending in other parts of the budget.

The Abe cabinet deserves some credit for reining in growth in the fiscal 2015 budget, but unfortunately, the latest budget document does not tell the whole story. Just prior to adopting the 2015 budget, the cabinet also approved a ¥3.1 trillion supplementary budget for fiscal 2014. Despite efforts to minimize allocations for lengthy public-works projects, the government predicts that ¥1.2 billion of this stimulus spending will carry over to fiscal 2015. Even granting its projection of ¥400 billion in added tax revenue stemming from the stimulus, the net result will be a ¥800 billion increase in the primary deficit in fiscal 2015.

Cockeyed Optimism

To recap, the government began with a primary deficit of ¥16.1 trillion for fiscal 2015, according to Cabinet Office projections. If we add to this the ¥1.5 trillion in lost tax revenue resulting from the postponed tax hike, the deficit rises to ¥17.6. The Ministry of Finance managed to scrape up ¥1 trillion through spending cuts and another ¥600 billion through accounting gimmicks, bringing the deficit down to ¥16 billion. However, if we add ¥1.2 trillion in spending carried over from the supplementary 2014 budget, then even with the projected ¥400 billion in added tax revenue, we end up with a primary deficit of ¥16.8 trillion.

This is just barely within the ¥16.9 trillion limit that the government must honor if it is to meet its goal of halving the ratio of the primary deficit to GDP. With even a slightly larger carryover from the supplementary budget, for example, the government would fall sort of its goal. One assumes, therefore, that Asō was factoring in about ¥400 billion in potential savings at the local level (resulting from a combination of budget trimming and increased tax receipts relating to the supplementary budget) when he optimistically announced that the government was on track to meet the target.

In any case, the foregoing analysis casts serious doubt on the claim that the fiscal 2015 budget allows the government to reach its goal of halving the primary deficit ratio despite postponement of the consumption tax hike. A more accurate assessment would be that the Finance Ministry, driven by political considerations, has used every trick in the book to create the appearance of meeting that goal.

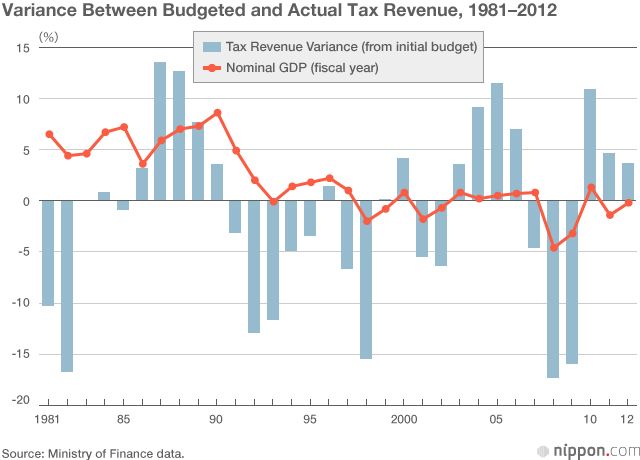

In short, Japan’s outlook for achieving its fiscal sustainability targets is doubtful, even if we accept the government’s revenue estimates. In any case, such predictions are notoriously unreliable owing to vagaries of the global and domestic economy, as epitomized by the 2007–8 financial crisis. The graph below charts the rate of variance between the tax-revenue estimates in the government’s initial budget and confirmed tax revenues between 1981 and 2012. In 10 of those 30-odd years, tax receipts fell short of budgeted revenue by 5% or more. On 17 occasions the government overestimated tax revenue by a margin of 1% or more.

The budget plan recently approved by the cabinet estimates fiscal 2015 tax revenues at ¥54.5 trillion. On a settlement basis, this would equal the peak of ¥54.4 trillion reached before the asset bubble collapsed. If actual tax receipts were to fall short of the estimate by 5%, it would mean a shortfall of ¥2.7 trillion, which would put the goal of halving the primary deficit out of reach.

Tough Choices Ahead

Amidst all of this, Prime Minister Abe has renewed the government’s pledge to generate a primary budget surplus by 2020. With this goal in mind, the cabinet and the ruling party are at work on a new fiscal reform plan slated for release this coming summer. They will have their work cut out for them. In the medium- and long-term estimates released last July (which were predicated on an October 2015 tax hike), the Cabinet Office projected a fiscal 2020 primary deficit in excess of ¥10 trillion, even assuming that the rate of economic growth accelerates to 3%–4%.

As this demonstrates, economic growth, while important, will not be sufficient to put the nation’s finances on a sustainable trajectory. To begin with, the government needs to implement the planned consumption tax hike—now scheduled for April 2017—without fail. It also needs to tackle social security reform and consider the possibility of further tax increases as part of any viable fiscal rehabilitation plan. In addition, it must include in its plan a process chart and time schedule specifying spending cuts in each area of the budget, any additional tax hikes, and the timing of each of these measures.

A Matter of Political Will

Japan’s baby boomers continue to age. By 2025, the youngest of the boomers will be 75, and healthcare costs can be expected to skyrocket. Faced with this demographic time bomb, Japan has no choice but to rein in pension and health-care expenditures, most of which are legally mandated. This will necessitate a number of politically difficult steps, such as raising the minimum age for receipt of pension benefits, adopting a formula that would reduce benefits relative to the cost of living under deflationary or inflationary conditions, and propping up the health insurance system by instituting fixed copayments or increasing beneficiaries’ coinsurance share.

In Democracy in Deficit: The Political Legacy of Lord Keynes, James Buchanan and Richard Wagner stress that in real-world democracies, where politicians need to win elections, tax cuts are always much easier to pass than tax increases. They argue that for this reason a constitutional provision requiring a balanced budget is the only way to avoid government bloat and maintain healthy finances over the long term. Given the delicate politics of taxes and social security, Abe is to be commended for reaffirming the government’s commitment to the fiscal reform targets adopted in 2010.

Nonetheless, as Japan greets the seventieth anniversary of the end of World War II, it faces the possibility of another historic debacle in the form of financial insolvency. Where fiscal rehabilitation is concerned, the next few years will be a crucial test of the Abe cabinet’s political will.

(Originally written in Japanese and published on February 5, 2015. Banner photograph: Finance Minister Asō Tarō briefs the press on the fiscal 2015 budget at the Prime Minister’s Official Residence, September 12, 2015.)

consumption tax Fiscal crisis public debt social security reforms primary deficit ratio fiscal 2015 budget plan