Tax and Reform: Dealing with Japan’s Runaway Debt

The Barriers to Budget Balance in Japan

Politics Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

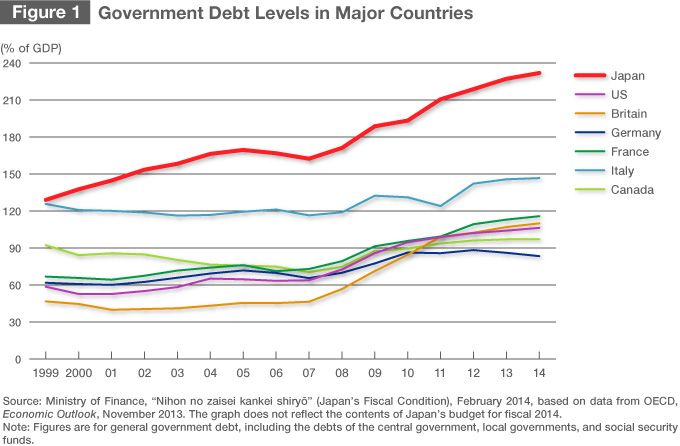

Japan’s Level of Public Debt Towers Over Other Countries’

According to comparative international statistics from the Organization for Economic Cooperation and Development, Japan’s public debt (“general government” debt, including the debts of local governments and social security funds) as of 2012 was equivalent to 218.8% of the country’s gross domestic product. This figure is more than twice that of the United States (102.1%) and about 1.3 times that of Greece (167.3%), whose 2010 debt crisis attracted global attention; it is the highest debt level among the OECD member countries.

If we focus just on the changes in Japan’s public debt over time, we find that the ratio to GDP as of 2012 had already topped the level reached in fiscal 1944 (April 1944–March 1945), after eight years of waging all-out warfare following the outbreak of the second Sino-Japanese War in 1937. The huge government debt that accumulated during the war years was impossible to pay off by ordinary means; in the end it was cleared away by the galloping inflation that continued through the years after the end of the war—in effect, an “inflation tax.” Over the five years from 1944 to 1949, when the rapid inflation came to an end, wholesale prices rose by a factor of 90. In other words, the value of the government’s debt, which was in the form of bonds with fixed face values, fell to one-ninetieth of its previous level. The losses were effectively borne by the members of the general public who owned government bonds either directly or indirectly through financial institutions.

Thanks in large part to the effect of this inflation tax, the ratio of public debt to gross national product plunged to 14.0% by fiscal 1950. The figure declined further during the period of rapid economic growth that got underway in the latter part of the 1950s, and as of fiscal 1964 it was only 4.4%. After that, though, the figure started rising again, and since the 1990s it has been climbing at an accelerated pace.

An Aging Population and Extreme Rigidity in Public Finances

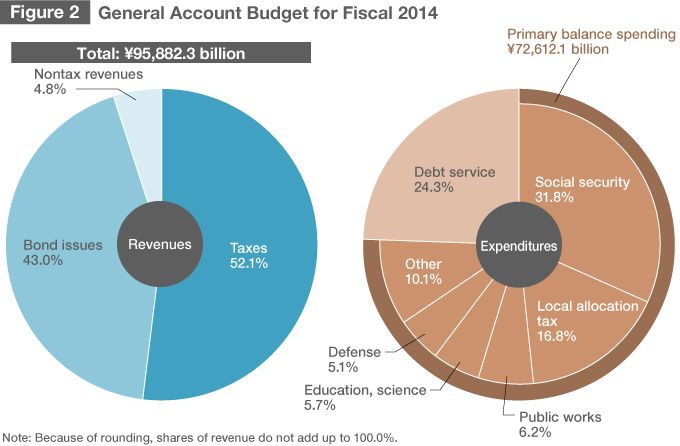

Japan’s public debt has already reached a crisis level, and what makes the situation even graver is the fact that the government continues to run up deficits year by year. Under the budget for fiscal 2014, enacted by the National Diet on March 20, the government is planning to borrow ¥41,250 billion, a figure that amounts to 43.0% of the expected total revenues of ¥95,882.3 billion. The primary balance (the balance between revenues excluding new borrowing and expenditures excluding debt service) will be in the red to the tune of ¥22,611.1 billion; this shortfall will have to be covered by an equivalent increase in government debt, an increase amounting to almost 5% of GDP.

There is also a problem in the structure of expenditures. Debt service and social security costs, categories of spending over which the government has little discretion, account for 24.3% and 31.8%, respectively, of expenditures; together these nondiscretionary appropriations make up 56.1% of the total for the year. In the latter part of the 1960s, as the government’s debt started to climb, the Ministry of Finance focused on the problem of fiscal rigidity—the rise in the level of nondiscretionary spending—and proclaimed the need to correct it. But as of fiscal 1968, when the ministry was waging its campaign against this rigidity, debt service and social security accounted for just 3.5% and 14.1%, respectively, or a combined share of 17.5% (after rounding) of total spending. By comparison with those days, Japan’s public finances have become rigid to a much more extreme degree.

The rapid aging of Japan’s population is the fundamental factor underlying the present state of the country’s public finances. Social security expenditures are the main cause of the swelling of government spending, and the bulk of these expenditures are used for senior citizens in the form of pensions, medical care, and long-term care. These benefits for the elderly account for 73.9% of social-security-related appropriations in the fiscal 2014 budget.

The Democracy Trap in the Way of Fiscal Rehabilitation

It is politics, however, that has caused this situation to turn into a fiscal crisis. From the late 1960s, when the government debt started to swell, through the present, there have been repeated attempts to repair Japan’s public finances, including the Ministry of Finance’s campaign against fiscal rigidity. Among the efforts that have been undertaken for this purpose, three stand out: the introduction of the consumption tax, an across-the-board 3% levy on sales, under Prime Minister Takeshita Noboru in 1989, the hike of the consumption tax rate to 5% under Prime Minister Hashimoto Ryūtarō in 1997, and the move to hike the rate to 8% in April 2014, which was enacted under Prime Minister Noda Yoshihiko in 2012 and is being implemented under Prime Minister Abe Shinzō. The administrations that decided on these moves were all trounced by the voters at the next election.

This experience highlights the difficulty of fiscal rehabilitation in a democracy. Since individual voters bear only a fraction of the cost of the benefits they receive from the public purse through the taxes they pay, their political judgment tends to be biased in favor of increased benefits for themselves, meaning more government spending. And when a tax hike is proposed, people tend to throw their support behind politicians who glibly assert that wasteful spending by others is the cause of the deficit and claim that the hike will not be needed if the waste is eliminated.

The Loophole in the Public Finance Act

Over the long course of history, people have come up with various devices aimed at avoiding this “democracy trap.” Simply put, these have been tools for making commitments—deliberately setting limits on the discretionary scope of democratic governments.

One example of such a commitment tool is a currency system based on the gold standard or a fixed exchange rate. Under the gold standard, the value of a currency and the amount of it in circulation are linked to the country’s reserves of gold, and this link acts as a brake on government spending and fiscal deficits that may result in international payments deficits (outflows of gold). A commitment to maintaining a fixed exchange rate has the same sort of effect.

Another sort of commitment tool is the adoption of constitutional or legal constraints. In the case of postwar Japan, for example, the Public Finance Act of 1947 sets the basic rules for government finances, including the following provision in Article 4: “The expenditure of the state shall have its financial sources in revenue other than public loans or borrowing.” But the law continues as follows: “It is provided, however, that as concerns the financial source of public work expenditures, investment and advances, it is authorized to issue public loans or to make borrowings, within the limits of the amounts sanctioned, as the result of a decision by the Diet.”(*1) This has provided a critical loophole. Ever since fiscal 1966, for almost 50 years, so-called construction bonds have been issued under this exemption.

On a more basic level, the effectiveness of this sort of law as a government commitment tool is limited inasmuch as the law itself can be amended by a group with a majority in the legislature. This limitation is particularly clear in the case of a parliamentary democracy like Japan’s, where the party or parties with a legislative majority get to rule the government. In Japan’s case, aside from the construction bonds issued under the exemption noted above, large amounts of deficit-financing bonds have been issued by having the Diet pass enabling legislation providing for exceptions to the Public Finance Act every year.

The Role Played by the Prewar Genrō

A third type of tool for committing the government to fiscal probity is the yielding of authority over public finances to a neutral body that has at least a relative degree of independence from democratic controls. One example of such an arrangement that seems to have been effective is the informal system of oversight by the senior statesmen known as genrō in prewar Japan. The 1889 Meiji Constitution (Constitution of the Empire of Japan) did not provide for genrō, but the term came to be applied to a group of leaders who had wielded great political influence since the Meiji Restoration of 1868 and whom the emperor consulted particularly when naming a prime minister. The veteran leaders in question were Itō Hirobumi, Yamagata Aritomo, Kuroda Kiyotaka, Inoue Kaoru, Saigō Tsugumichi, Ōyama Iwao, and Matsukata Masayoshi.

In the early twentieth century, as Japan’s political parties gained strength and the characteristic democratic pressure for the swelling of the budget increased, the genrō served as a bulwark against this pressure. The Russo-Japanese War of 1904–5 was a major conflict involving military expenditures equivalent to 68% of Japan’s 1903 GNP, and though Japan was victorious, it did not win reparations under the peace settlement (as it had after the Sino-Japanese War of 1894–95), and so the government was left with a huge debt to service.

Despite this financial tightness, the government came under pressure from three directions for increased spending: from the army and navy, whose victory in the war had boosted their say, from the Home Ministry and Ministry of Railways, which sought money to improve the nation’s industrial infrastructure, such as railways, ports, and telegraph lines, and from the Rikken Seiyūkai (Friends of Constitutional Government), the most powerful political party, which was seeking to provide patronage benefits for local constituencies.

In the end, though, government spending after the war was held in check, the primary balance was kept in the black, and the government debt that had swollen during the war was reduced. This was made possible by the backing the Ministry of Finance received from the genrō in its fight against spending hikes. For example, in 1911 Inoue Kaoru and Shibusawa Eiichi, an influential business leader, submitted an opinion paper to Prime Minister Saionji Kinmochi calling for fiscal management based on (1) no foreign borrowing, (2) redemption of outstanding government bonds, and (3) streamlining of government organs. And the Ministry of Finance, with Inoue’s support, succeeded in cutting the public works spending demanded by the Home Ministry and Seiyūkai.

The genrō displayed several key characteristics in their role as an unofficial organ of the state. First, they were isolated from democratic control, since their positions did not depend on elections. Second, their status was effectively for life. And third, they were able to exercise influence on both the government and the military, which were separate loci of power under the Meiji Constitution. Thanks to these characteristics, they were unaffected by the democratic pressure for spending growth, and they were able to offer opinions on fiscal affairs from a long-range perspective, with their eyes on the national interest rather than the interests of particular groups. It was after the death of Saionji Kinmochi, who joined the ranks of the genrō during the Taishō era (1912–26) and was the last of them to survive, passing away in 1940, that Japan rushed down the road to financial ruin; this may be seen as symbolic of the role that the genrō had played.

Leadership by Elected Politicians Is Not the Answer

In today’s Japan, as noted above, public finances are already in a grave state in quantitative terms. On top of that, the commitment apparatus for restraint on government spending and fiscal deficits is not operating properly, and political forces are working to make it even weaker. Needless to say, Japan is not operating under the gold standard or a fixed exchange rate, and these are not appropriate options.

Under these circumstances, domestic legal and institutional commitments have a major role to play. Over the past half century, however, the Public Finance Act has almost completely failed to function as a commitment tool. Furthermore, the current administration is carrying on with the “politician-led government” espoused by the Democratic Party of Japan when it was in power (2009–12), moving away from the idea of entrusting particular areas of decision making to neutral organs independent of political control.

The simplistic notion that Japan will benefit by having elected politicians call the shots seems to have won broad support not just in the government and the ruling and opposition parties but also among political commentators. As this indicates, the crisis in Japan’s public finances is a far-reaching problem.

[Originally written in Japanese on March 20, 2014. Title photo: Japan’s Deputy Prime Minister and Minister of Finance Asō Tarō and US Federal Reserve Board Chair Janet Yellen (center), along with Bank of Japan Governor Kuroda Haruhiko (right), at a meeting of the Group of 20 finance ministers and central bank governors in Sydney, Australia, on February 22, 2014. Photo by Reuters/Aflo.]

(*1) ^ English translation from http://www.mof.go.jp/english/pri/publication/pp_review/ppr015/ppr015b.pdf.

social security consumption tax GDP OECD budget crisis primary balance finance inflation Tetsuji Okazaki public debt general account construction bonds