Tax and Reform: Dealing with Japan’s Runaway Debt

Clock Running Down on Social Security Reform

Politics Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Making Social Welfare Reform a “Fourth Arrow”

Japan’s “Abenomics” strategy continues to pursue the goal of revitalizing the economy with its “three arrows” of fiscal stimulus, monetary easing, and a growth strategy driven by structural reforms. Returning to sustained economic growth, however, will first require Japan to put its mounting public debt in check to regain a sound fiscal footing.

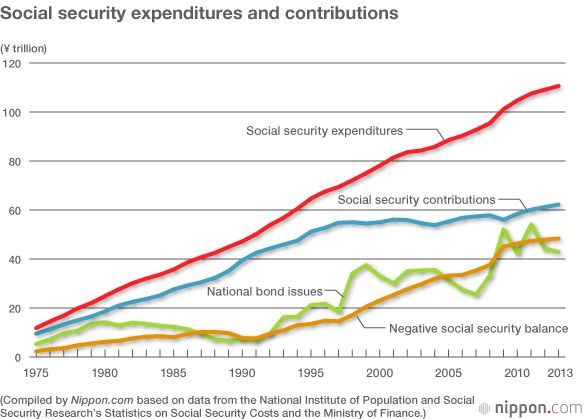

The graying of Japan’s population is deeply reflected in public spending on social security programs, which increased on average by ¥2.7 trillion annually over the 20 years to 2013. During the same period, social insurance premiums, which are tallied according to household income, increased by just ¥800 billion a year, being held down by stagnant wages. This has resulted in an annual shortfall of nearly ¥2 trillion that continues to be subsidized by budgetary outlays at the national and local levels. Tax revenue and economic growth have remained flat, making public bond issues the lone means of covering increases in social security benefit payments.

The government, in a bid to rebuild public finances, will increase the consumption tax from 5% to 10% in two steps by 2015 (the first increase, to 8%, went into effect on April 1, 2014). The government expects the 5-point hike to add ¥13.5 trillion annually to public coffers, but rising social security expenditures mean that the amount will only cover shortfalls for five years. Without reform, social security will have to rely indefinitely on government bonds to remain viable. Japan’s national debt is already more than twice GDP, and confidence in government bonds is among the lowest among developed nations. Further inflating the debt will have unavoidable consequences.

As part of fiscal reforms, the cabinet of Prime Minister Abe Shinzō established the medium-term goal of putting the nation’s primary balance in the black by 2020. To accomplish this, the government must swiftly carry out what amounts to a “fourth arrow” of reforms targeting the social welfare system, a major driver of government debt.

Short-Sighted Politics Slowing Reform

The current public pension and healthcare systems were first devised toward the end of Japan’s period of high-speed economic growth cresting in the 1960s. They were based on an assumption of sustained economic expansion, which during this time averaged 10% annually. Population ratio estimates for senior citizens were set at an unrealistically low 20%, even for the year 2050, when the elderly population is projected to peak. This is only half of current, more realistic, estimates—a misjudgment that shows a lack of realistic thinking among policymakers of the day. Despite widespread social and economic changes since then, lack of sufficient governmental action to shore up social security finances has resulted in the problem being kicked down the road for coming generations.

This “generational imbalance” extends beyond growing the debt to meet current obligations to social welfare recipients. Compared to future obligations, the public pension system is estimated to have a shortfall in contributions of nearly ¥480 trillion, almost equal to Japan’s GDP. The amount, however, is tabulated “Off balance sheet” and not included in official calculations. Nonetheless, it will be up to future generations to pay this back.

In August 2013, the government’s National Council on Social Security System Reform issued its final report. Despite the acute risks facing social security, the council firmly backed the current system and presented only modest ideas for reform within the existing framework.

The public pension system is widely believed to be impervious to bankruptcy. This is based on the pretense that, unlike the private sector, the government can support the system by raising taxes. In reality, though, the government’s lack of resolve to adequately use its power of taxation has caused the red ink to swell.

An absence of political will has also held back social security reform. Concerned about short-term election outcomes, politicians have avoided the issue of reform, which is publicly unpopular. For instance, the Ministry of Health, Labor, and Welfare, which oversees the social security system, has habitually avoided essential reforms by including unrealistic assumptions as part of its policies. For example, pension reform enacted in 2004 included the extreme assumption of sustained annual investment returns of 4.1% over the long term. This created a scenario, the “100-year safe pension plan,” where steady increases of payments into the pool over the long term would sustain the pension system without need for ambitious reform. A slightly revised version of this policy was also included as part of 2014 budget reforms.

Postponing Pension Eligibility

Reducing benefit payments and raising insurance premiums are fundamental ways to improve the financial stability of a pension system. Lowering the ratio of pensioners is another way to control additional increases in payouts. In the current system, annual adjustments for inflation are the sole way benefits are kept from sliding in nominal terms. To date, no adjustments have been made during deflationary periods. These restrictions should be done away with and automatic adjustment mechanisms implemented.

Raising the age at which pensioners can start receiving benefits will also work to improve budget woes by extending the period workers pay into the system and reducing the payment period. The pension eligibility age in Japan is slated to be raised to 65 in 2025 for men and 2030 for women. This is excessively low when compared to the average of 67–68 in the United States and Europe. Given that Japan boasts one of the longest average life expectancies in the world, the government should aim to raise the eligibility age to at least 70.

All developed nations face the issue of graying populations, but one benefit Japan enjoys is high motivation for employment among its older citizens. 2010 employment figures for men 60–64 years old showed Japan, at 76%, well above the United States (59%) and Germany (56%). This can be attributed to the longevity of its citizens as well as the high standard of health compared to similarly aged populations in other countries. Labor practices favoring older workers also play a role. Regardless of the reasons, the environment is favorable for a higher retirement age and should be taken full advantage of.

Hospitals or Nursing Homes?

By 2050, senior citizens will make up nearly 40% of the population, with two-thirds being 75 and older. As the senior population continues to live longer, health and nursing care costs for this superannuated cohort will form the largest increase in benefit payments. The Health Ministry estimates that this age group will account for three-quarters of all increases in social security benefits from 2010 to 2025.

A deficiency in coordination between hospitals and clinics is a major issue affecting how medical resources are distributed. Japan has 13.4 hospital beds per 1,000 people, considerably more than the 3–8 beds available in Europe and the United States. However, a large number of these beds are full due to hospitals being increasingly burdened with long-term care of elderly patients. This has created a situation where ambulances often struggle to find facilities with available bed space. Even hospitals providing specialized treatment must devote a considerable amount of resources to patients with minor ailments, hindering their ability to provide adequate treatment in severe cases.

In Europe, patients with minor conditions are mainly treated at clinics by general practitioners, so called “family doctors.” These family practitioners serve an important role as gatekeepers by referring patients needing more specialized care to hospitals. While GPs make up half of all physicians in many other OECD member nations, in Japan their numbers are exceedingly small. As the number of elderly patients grows, many will need to be treated for multiple ailments. It is imperative to educate a greater number of GPs who can provide the basic care they need. Creating a clear division in roles, with local clinics treating minor conditions and hospitals focusing on specialized cases, would result in a better level of overall medical care. This would also reduce medical costs related to overlapping treatment at multiple facilities, testing, medication, and other factors that particularly impact aged patient care.

Medical Expense Reform Urgently Needed

Reform of the way medical costs are calculated is also needed. Traditionally, costs for such services as examinations, tests, and prescriptions are set according to individual procedures, with remuneration for doctors being based on a fee-for-service system. This has led to a high ratio of hospitals and clinics with costly diagnostic equipment, creating conditions conducive to overdiagnosis and overtreatment of patients. For example, in Japan there are 101 CT scans per 1 million people, while in other developed countries there are between 20 and 40. Basing doctor fees on a comprehensive payment system according to treatment of specific conditions would improve medical care by acting as a strong incentive for institutions to streamline the care they provide.

Allowing the effective use of mixed treatments is another pillar of reform for reducing ballooning healthcare costs. This would enable public health insurance to partially cover treatments not listed in the public billing package (something not allowed under the current system, in which patients choosing optional treatments must cover 100% of costs). Japan’s health insurance system was created at a time when acute and contagious diseases, such as tuberculosis, accounted for a majority of medical costs; with today’s aging society, the shift is heavily toward chronic disorders. The overall framework of healthcare is moving from a public service, somewhat similar to police and fire departments, toward a more customized and individual type of care.

Medical costs will continue their upward trend as the population grays and new medical technologies emerge. A choice between standard healthcare covered by public insurance and “additional cost” procedures on the open market needs to be available for the entire population. Unless medical costs are kept at a sustainable level, social health insurance runs the risk of ceasing to function altogether.

Until now, the opinion among many in the medical industry has been that advanced medical procedures, such as organ transplants and customized genetic treatments, are too expensive and should be excluded from social insurance coverage. There is a rising need to rethink what constitutes basic coverage and what should be additional-cost procedures.

Optional treatments are controlled by supply and demand, with prices being set in line with the effectiveness of the procedure and patient satisfaction. A market could potentially arise for an increasing variety of new medical services being developed, thus creating manufacturing and employment opportunities. And as these treatments become mainstream, they could be brought under the social insurance system and their use made more universally widespread.

Growth Strategies for the Silver Market

The long-term care insurance system was established in 2000, and unlike medical insurance, it features a high degree of flexibility. For example, publicly provided insurance will cover nursing care service up to twice a week. Using long-term care insurance, patients have the option of paying out of pocket to increase this to three.

Under the system, however, fees for individual care services are rigidly defined, and recipients are denied the option of choosing alternative higher-level services, even when at comparable cost. Abolishing price regulations would increase public and private nursing care options, improve profitability for nursing care companies, and increase wages for care providers.

Live-in nursing care, such as that provided in publicly run nursing homes, and in-home care are the two main services covered by long-term care insurance. Live-in nursing care facilities are more expensive to maintain, resulting in a persistent shortage of slots for residents. One way to address this shortage would be to construct communal living facilities for the elderly, such as group homes and assisted living facilities, in combination with in-home nursing care services. Communal living facilities would alleviate the current shortage of long-term nursing care facilities. Centralizing care, meanwhile, would also increase efficiency by reducing the need for caregivers to attend to seniors living in different locations. Over the medium term, promoting combined facility-based and in-home care will be an important issue for society as it ages.

For the government, the growing burden on social welfare of Japan’s rapidly graying society sits like a dark cloud on the horizon. For the private sector, however, the graying of society promises a sturdy customer base—a so-called silver market—in the fields of health and nursing care. Institutional and regulatory reforms must be carried out to foster the market through increased availability of a wide range of medical and care services. Reforms must also serve to clearly define public- and private-sector roles. Developing the health and nursing care service industries will turn them into pillars of Japan’s growth strategy.

References:

Yashiro Naohiro. Shakai hoshō o tatenaosu (Rebuilding the Social Welfare System). Nikkei Publishing, 2013.

Suzuki Wataru. Shakai hoshō bōkokuron (How Social Welfare is Destroying the Country). Kōdansha, 2014.

Nishizawa Kazuhiko. Zei to shakai hoshō no bappon kaikaku (Fundamental Tax and Social Welfare Reform). Nikkei Publishing, 2011.

(Originally published in Japanese on April 8, 2014. Banner photo: Residents and caregivers at a nursing care facility in Japan. Photo by Jiji Press.)

social security budget Health medicine public debt senior citizens insurance