Corporate Governance: Can Japanese Business Adapt to a New Era?

Toward a Multi-Stakeholder Model of Corporate Governance

Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Corporate governance has come under intense scrutiny in Japan since the collapse of the asset bubble in the early 1990s. One underlying factor was the drop in corporate performance accompanying the shift to slow economic growth. The governance structures that had functioned so well during the period of rapid growth—distributing the benefits of growth not only to executives but also to employees, shareholders, and creditors—were no longer delivering, and stakeholders grew dissatisfied. Another factor was the unprecedented number of corporate failures and scandals that began to make headlines during the post-bubble era, amid the pressures of the recession and financial crisis of the 1990s.

Closely tracking this growth in public concern, the government undertook a series of regulatory reforms starting around 1997. Thanks to these and other factors, the face of Japanese corporate governance is changing substantially. As we shall see, however, much remains to be done to make Japanese corporations not only more efficient and competitive but also more socially responsible and sustainable.

Structural Reform in the Era of Slow Growth

Moves to reform corporate governance at the statutory level picked up momentum in the second half of the 1990s, as business performance languished and the government searched for ways to revitalize Japanese industry.

In 1997, in an effort to boost performance incentives, the Diet amended the Commercial Code to allow companies to offer stock options to executives. In the same year, it amended the nation’s antitrust legislation to hasten restructuring, as by relaxing the old prohibition on pure holding companies. The stock market deregulation of 2001 eliminated most restrictions on stock repurchasing, and another amendment of the Commercial Code instituted the “company with committees” system in 2002. The Diet passed further governance reforms in 2005, when it enacted a Companies Act as a statute independent of the Commercial Code with the aim of modernizing and systematizing corporate law.

In 2010, the Companies Act Subcommittee of the Justice Ministry’s Legislative Council began deliberations on a new set of reforms, including a requirement that listed companies appoint outside directors. Although the revised Companies Act of 2014 did not make such appointments mandatory, it did incorporate a provision requiring companies to provide a compelling reason if they chose not to appoint an outside director.

These legal measures have been supplemented by such guidelines as the 2014 Japanese Stewardship Code for responsible institutional investing and Japan’s Corporate Governance Code, adopted this year. The former focuses on the need for dialogue between investors and business executives, while the latter is aimed at sustainable medium-to-long-term growth in corporate value through adherence to five basic principles: guarantee of the rights and equal treatment of shareholders, cooperation with stakeholders other than shareholders, information disclosure and transparency, fulfillment of the board’s responsibilities as outlined in the code, and dialogue with shareholders.

Reflecting these systemic reforms, corporate governance in Japan has undergone quantifiable changes in three key areas.

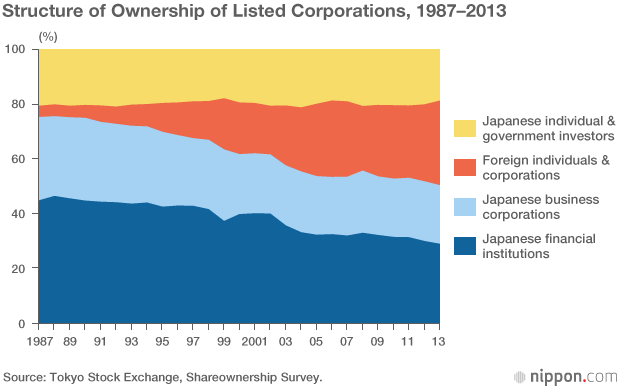

The first is a long-term shift in the ownership structure of listed companies, illustrated below. The share of stock owned by foreigners (corporations and individuals) rose from a mere 4% in 1987 to 30.8% in 2013, while the share controlled by Japanese financial institutions and business corporations fell substantially.

The second quantifiable change is an increase in the number of Japanese companies appointing outside directors. According to a survey by the Japan Association of Corporate Directors, of those companies listed in the first section of the Tokyo Stock Exchange, just over 30% had outside directors in 2004, when the survey was launched. That ratio rose to more than 50% by 2011 and hit 74% in 2014.

The third change is the increase in the adoption of executive incentive compensation plans. The number of Japanese companies making use of stock options has grown steadily since the system was instituted in 1997. As of the most recent survey, the number of such corporations on the TSE had surpassed 700. Similarly, the use of performance-linked remuneration has spread as well, with about 500 listed companies reporting the use of such a system.

The Stakeholder Society and CSR

While growth in corporate value is an obvious goal and indicator of corporate management, another extremely important aspect of governance is how equitably and efficiently that value is shared among stakeholders. “Stakeholders” in this context encompasses not only shareholders but everyone with a direct or indirect stake in a company, including its creditors, the employees who work there, the customers who buy its products, the suppliers that provide it with materials, and the residents of the community where it is located.

Jean Tirole, winner of the 2014 Nobel Prize in economics, maintains that the mission of management should be to “maximize the sum of the stakeholders' surpluses,” in keeping with the concept of the “stakeholder society.” Moreover, he calls for mechanisms to protect noncontrolling stakeholders, including systems for distributing surpluses in such a way as to compensate specific stakeholder groups affected negatively by management decisions.

Corporate social responsibility, or CSR, is essentially the application of the “stakeholder society” concept to business management. According to the European Commission’s 2001 Green Paper “Promoting a European Framework for Corporate Social Responsibility,” CSR can be defined as “a concept whereby companies integrate social and environmental concerns in their business operations and in their interaction with their stakeholders on a voluntary basis.”

Socially responsible investing, or sustainable and responsible investing (SRI in either case), is an important tool for promoting CSR. SRI can take three different forms: (1) screening, which channels investment into socially responsible companies based on outside assessments; (2) shareholder activism, which uses resolutions, dialogue, and similar tools to influence management decisions; and (3) community investment, which channels capital directly to needy communities through financing and business investment.

According to the Forum for Responsible and Sustainable Investment, a US organization of professionals, organizations, and institutions involved in SRI, the total value of US assets invested according to SRI criteria has grown continuously over the past two decades, rising from $1.2 trillion in 1997 to $2.3 trillion in 2005, $3.1 trillion in 2010, and $6.6 trillion in 2014.

In Britain, meanwhile, investment in ethical funds and other SRI investment trusts has grown steadily, rising from a mere £300 million at the beginning of the 1990s to £3.3 billion in 2000, £6.0 billion in 2005, and £13.5 billion in 2014.

In Japan, organized SRI investing began in 1999 with the launch of five “eco funds,” but it has yet to gain serious momentum. According to the Japan Social Investment Forum, a nonprofit organization established to promote SRI in Japan, the total value of assets managed by responsible investment trusts was a mere ¥600 billion as of 2014, a small fraction of the sums recorded in the United States and Britain.

Given the increasing urgency of climate change and other global environmental issues, along with growing regional threats to security, safety, health, and human rights, the need for CSR and SRI can only grow. We must continue to strengthen and disseminate a model of corporate governance grounded in the notion of maximizing benefits to all stakeholders—from employees and investors to the local community, the global community, and the earth itself.

Toward Multidimensional Governance

Models of corporate governance predicated on shareholder supremacy, while seemingly consistent with current corporate law, are ill-equipped to take into account the long-term, social, and global ramifications of corporate activity. Business management responsive to the interests of a wide range of stakeholders is proving essential from the standpoint of corporate social responsibility.

It should be noted that under the traditional postwar Japanese corporate governance system, management decisions were largely guided by stakeholders other than shareholders, particularly the other companies in the keiretsu network and the “main bank” that provided financing. But this is not the model to which Japanese companies should aspire today. In a world in which companies’ business decisions—for example, those affecting emissions of carbon dioxide and other pollutants—can have global consequences, the narrow economic interests of a corporation’s suppliers, distributors, and creditors cannot point the way to responsible business management. Corporate engagement with and responsibility to stakeholders must expand to encompass the entire nation and, ultimately, all of humankind, including future generations.

What all of this points to is the growing need for a socially oriented model of corporate governance under which every aspect of business activity is guided and constrained by the imperatives of economic and social sustainability, most notably the need to stem environmental destruction and climate change (caused by human economic development) and equip our communities to prevent and respond to human and natural disasters.

Any serious examination of the issues of corporate governance must ultimately lead one to reflect on the basic nature and purpose of a corporation. As our corporate system evolves, the social and public aspects of the corporation are coming to the fore. The concept of the corporation is a social entity is already a proposition that demands recognition, and its influence is sure to grow in the years ahead.

(Originally published in Japanese on September 18, 2015. Banner photo: Tokyo Station flanked by the high-rise office buildings of the Marunouchi and Yaesu business districts.© Jiji.)environment corporate governance Corporate Management Companies Act outside directors stock options CSR SRI stakeholders