Revisiting Japan’s Lost Generation

Japan and the Lost Generation’s Looming Pension Crisis

Economy Politics- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

In Japan, the term Lost Generation refers to those who had the bad luck to graduate during the “employment ice age” of the 1990s and 2000s—after the collapse of the 1980s asset-price bubble—when companies sharply curtailed their annual recruitment of permanent employees. Having missed the narrow window for securing “regular” employment, many have been moving from one low-wage job to another ever since. Now ranging in age from around 40 to their early fifties, members of this generation will start retiring in another decade or so, and there are serious questions about the capacity of Japan’s public pension system to sustain them through old age.

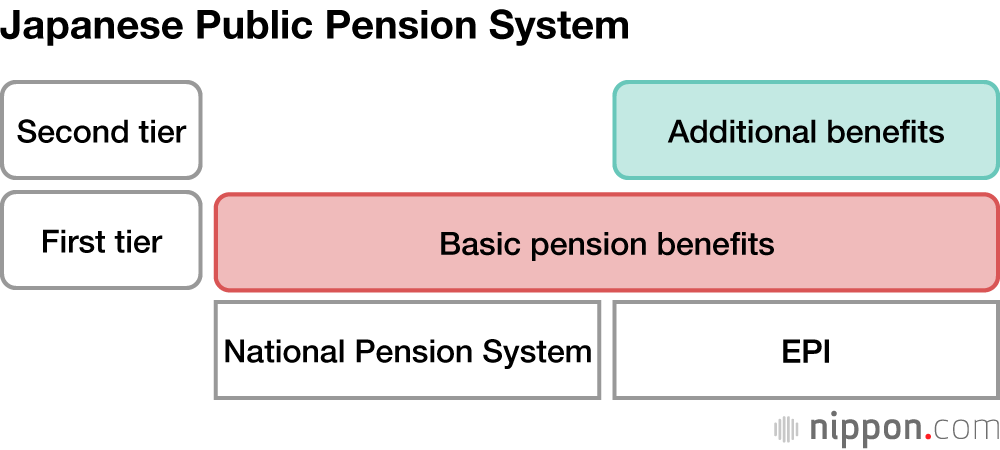

Japan’s Two-Tiered System

Japan has a two-tiered pension system. The first tier, the National Pension system, begins paying out the “basic pension” benefit to all registered residents, regardless of their jobs or employment status, when they reach 65. The premiums are the same for everyone in principle, as is the full benefit amount (based on 40 years of employment). The second tier, represented by Employees’ Pension Insurance (EPI), pays additional benefits in proportion to one’s average earnings while employed.

In principle, companies are required to enroll their employees in EPI and cover half of their premiums—a fixed percentage of their wages—with the remainder automatically deducted from their paycheck.. But many gig workers, freelancers, and other short-term workers are never enrolled in EPI. They are denied the earnings-related benefit and must pay the full National Pension premium themselves. The National Pension’s system of fixed contributions is regressive, with the burden falling more heavily on those that make less. As a result, many members of the Lost Generation either failed to enroll in the National Pension scheme or fell behind on their premiums. The government offers partial or full exemptions for low-income households, but lower contributions translate into lower retirement benefits.

Nonregular employees who manage to enroll in EPI are a bit better off, as their employers pay half of their premiums, but since their compensation is generally lower than that of regular employees, their earnings-related benefits are naturally lower as well.

For those who secure positions as regular employees, Japan’s public pension system does a fairly good job in guaranteeing a minimum basic income after retirement. The same cannot be said for nonregular workers. The Lost Generation will soon be grappling with the limitations of Japan’s pension system.

The system has undergone several reforms and revisions since the 1990s, but none of these have addressed the looming crisis facing the Lost Generation. One reason is that, with that group’s retirement age still years off, no one considered it an urgent policy issue. An even bigger reason may be that the problem does not seriously impact the pension system’s finances. While it is true that members of this generation—many of whom are poorly paid nonregular workers—are paying less into the system, their future benefits are tied to their total contributions and will therefore be low as well. As a result, there has been little economic incentive to undertake reforms targeting the Lost Generation.

Social Insurance and Welfare

A general point to keep in mind when discussing this issue is that the public pension system is a form of social insurance, a mutual assistance program whose benefits are limited to paid members. As such, it is under no obligation to help people who are not enrolled or have failed to keep up with their premiums. Viewed in the context of an insurance scheme, this exclusion can be justified in the name of fairness. But it betrays society’s core expectation of a public pension system, which is to guarantee everyone a minimum level of economic security in old age.

Social security experts may argue that this expectation confuses the function of poverty prevention with that of poverty relief. The function of a public pension system, they may say, is to prevent poverty in old age. The task of providing relief for impoverished seniors lies with public assistance, or welfare. Such rigid thinking is doubtless one of the factors that has kept the Lost Generation problem off the pension-reform agenda.

Mind you, some have made the case for reforming the pension system itself so as to eliminate the danger of falling into poverty in old age. In the early years of the twenty-first century, there was a proposal to replace the first tier of the pension system with a “minimum guaranteed pension” that would provide all senior citizens with a basic income. A key factor behind this recommendation was an alarming increase in the number of people who were failing to enroll in or pay into the National Pension plan. But the idea was scrapped in the face of objections that providing equal benefits to contributors and noncontributors would be unfair to the former, and further, that the added costs of such a program would necessitate a hefty increase in the consumption tax. Since then, policy makers have clung to the notion that it is up to public assistance, not the public pension system, to rescue low-income seniors from poverty.

Meanwhile, another systemic issue bearing on low-income seniors has come into focus. This concerns the “macroeconomic slide,” introduced as part of the 2004 reform of the public pension system. The macroeconomic slide is an indexing mechanism that automatically limits total payouts of retirement benefits to keep them in balance with revenue from contributions (supplemented by fiscal subsidies), even while the contribution rate of working people is held to a legal ceiling. The adoption of the macroeconomic slide was an important milestone in the government’s effort to ensure the sustainability of the pension system.

But there are two sides to everything. The 2004 reforms prevent unrestrained growth in pension premiums, but with the population aging and shrinking and economic growth sluggish, the macroeconomic slide limits benefit increases, resulting in lower real benefit levels. Moreover, because the EPI was on a firmer financial footing than the National Pension, the mechanism was designed to have a bigger impact on basic pension benefits (the first tier) than earnings-related benefits. As a consequence, it disproportionately affects those with a small or nonexistent earnings-related component. In either case, it is more bad news for the Lost Generation.

Too Little, Too Late

Scholars and policy makers cannot have been unaware of these problems. But until recently, there was no indication that they saw them as warranting systemic reform. Now, however, with the oldest members of the Lost Generation in their fifties and approaching retirement age, policy makers are beginning to appreciate the gravity of the situation.

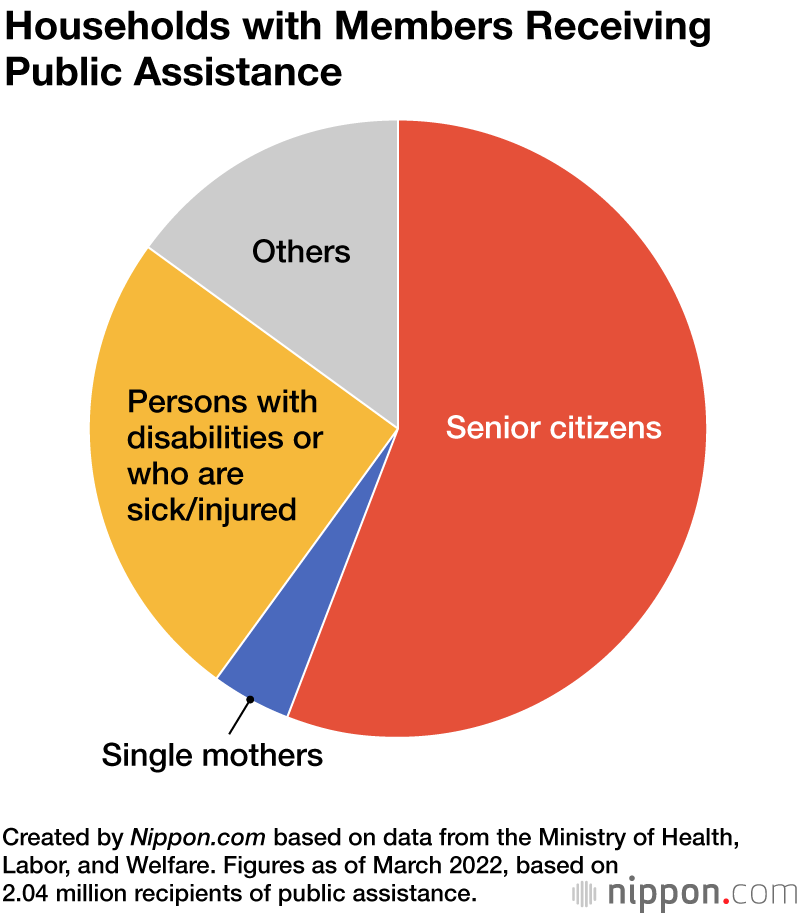

The problem concerns Japan’s public assistance program as well as its public pension system. Public assistance was designed primarily to provide emergency relief to those unable to maintain a minimum income level for whatever reasons and help them achieve independence. Low-income seniors are not generally expected to regain their independence, but people 65 or older currently account for more than half of those on public assistance, and their share is increasing rapidly. In short, public assistance is beginning to function as a supplementary pension.

However, unlike the public pension system, public assistance is funded entirely by the government (meaning taxes), and its fiscal base is inherently fragile. As underemployed members of the Lost Generation reach old age, more and more seniors will turn to public assistance to supplement their inadequate pension benefits and meager savings. It is doubtful that the current system will be able to bear the strain.

There are some signs of movement to address the shortcomings of the pension system. Three pertinent measures are currently being deliberated within the government. One is to expand the scope of the EPI to cover as many short-term nonregular employees as possible. The second is to extend the contribution period for the National Pension to age 65, from the current 60, in order to beef up total payments into the system. The third is to tweak the macroeconomic slide to better distribute the impact between the basic pension and the earnings-related component.

All these measures are steps in the right direction. But there are serious doubts as to whether they are sufficient to avert a pension crisis as the Lost Generation ages. In the absence of more far-reaching reforms, pension benefits will surely prove inadequate to the basic needs of the Lost Generation, and dependence on public assistance will skyrocket. That will place new strains on government finances. But judging from past behavior, our political leaders are unlikely to risk the wrath of voters by raising taxes to finance an expansion of welfare. Under the most likely scenario, the government will cover the cost with deficit-financing bonds, further eroding the wealth of future generations.

(Originally published in Japanese. Banner photo: A help desk for casualties of Japan’s “employment ice age” at an employment office in Saitama. © Jiji.)