The Nixon Shock of 1971 and Today’s “Cheap Japan”

Economy Politics- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Nixon’s Gamble

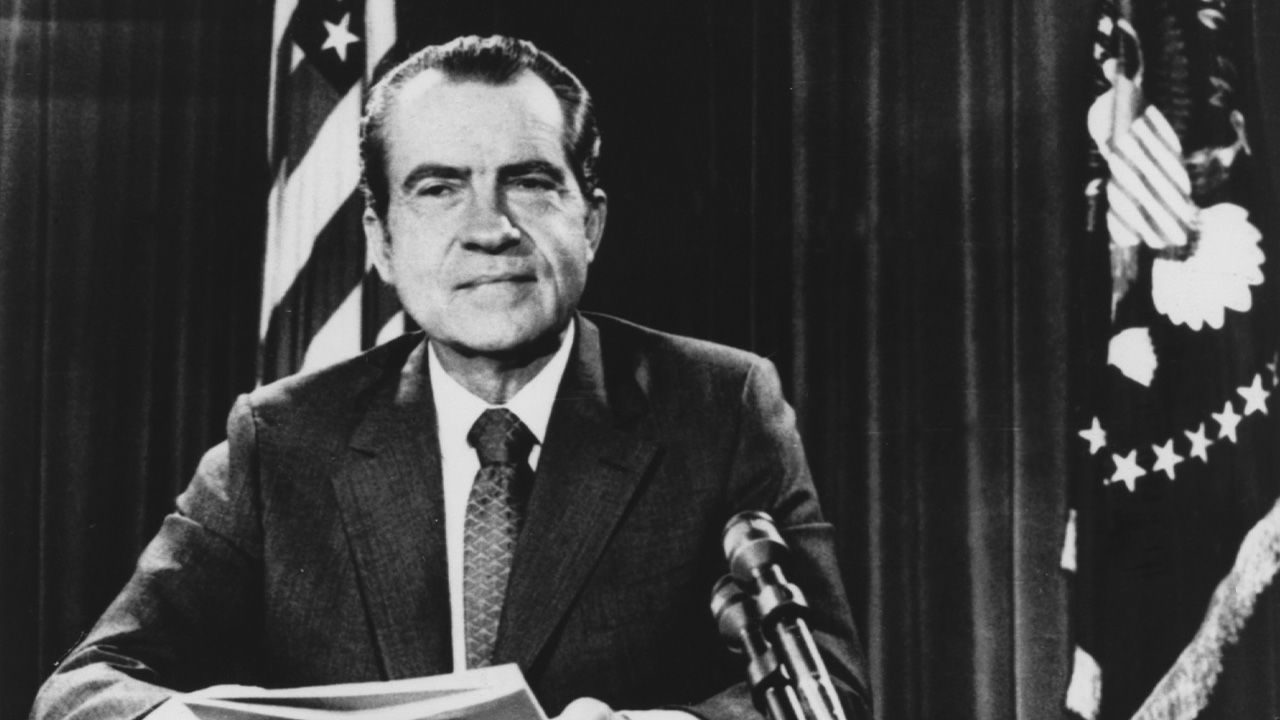

On August 15, 1971, 50 years ago this month, US President Richard Nixon delivered a televised address in which he announced the suspension of the convertibility of the dollar to gold. This move effectively brought down the post–World War II Bretton Woods international monetary system, under which the US dollar was convertible to gold at a rate of $35 dollars to the troy ounce and other major currencies were pegged at fixed rates to the dollar. It ended up paving the way to adoption of the current system of floating exchange rates.

The “Nixon shock,” as this sudden move was dubbed in Japan, was part of an economic policy package that included a freeze on prices and wages and the imposition of a 10% surcharge on imports. The United States at the time was struggling under the financial burden of the Vietnam War, which was making the government’s “guns and butter” spending policy untenable. Both inflation and unemployment were on the rise, and the swelling deficit in the balance of payments was sapping international confidence in the dollar. Nixon, a schemer, was gambling that his surprise package would bring all these problems under control.

For several months before Nixon’s August 15 address the greenback had been under selling pressure in European markets, and some countries with strong currencies, such as West Germany, had switched to floating exchange rates. By contrast, Japan’s monetary authorities were firmly determined to maintain the fixed rate of ¥360 to the dollar that had been maintained for over 20 years, and they had adopted an eight-part program aimed at preventing the yen from appreciating, including steps to open the Japanese market wider to imports.

The Emperor’s Observation

When Nixon dropped his August 15 bombshell, the market had already opened in Japan on the morning of August 16. Among officials in Tokyo, opinions were split on whether to close the foreign exchange market or to leave it open, and confusion prevailed within the administration. But one senior personage observed the situation calmly, namely Emperor Hirohito (posthumously Emperor Shōwa). On August 20, Finance Minister Mizuta Mikio visited the emperor at Nasu Imperial Villa, his summer residence in the mountains north of Tokyo, to make a presentation. According to Mizuta, the emperor questioned his suggestion that revaluation of the yen would cast a deep shadow on the Japanese economy. The finance minister paraphrased him as declaring, “I think that revaluation would be a good thing, raising the international standing of the yen. Doesn’t the public need to be informed of this positive aspect?” The emperor’s observation was based on his experience of the prewar years of floating exchange rates as Japan’s young sovereign.

It presently became apparent that Washington’s aim was to adjust the existing set of exchange rates through international agreement. For Japan, the Americans proposed a revaluation on the order of 25%. The Japanese authorities found themselves forced to float the yen, but they intervened in the foreign exchange market to limit the extent of its rise—a policy that German Finance Minister Karl Schiller mocked as a “dirty float.”

After several failed attempts at reaching an international agreement, the finance ministers of 10 major countries met in mid-December at the Smithsonian Institution in Washington DC, where they agreed on a new set of exchange rates for their currencies. The yen was set at ¥308 to the dollar, a hike in value of 16.88% over the previous rate. This was the largest margin of revaluation among any of the participating countries.

Pressure Behind the Scenes

This margin was larger than many in Japan had expected, even though Finance Minister Mizuta had talked US Treasury Secretary John Connally down from the 25% hike for which he had earlier called. Informed of the outcome, Prime Minister Satō Eisaku wrote in his diary, “I think the substantial revaluation will invite a substantial economic downturn; my concern is that it not be too big.” But the next day, prices on the Tokyo Stock Exchange were up. “It’s a bit hard to judge what’s what,” wrote the prime minister.

The new set of fixed exchange rates adopted late in 1971 did not hold up for long. The US dollar came under renewed pressure, and by the spring of 1973 all the major currencies had been floated. Even after the shift to floating rates, however, the Japanese continued to fear the effects of currency appreciation. Whenever the value of the yen headed up, the monetary authorities bought massive amounts of dollars in the foreign exchange market to dampen the rise. The result was excessive liquidity in the domestic economy, which pushed up both consumer prices and real estate values. The oil crisis that struck in October 1973 exacerbated the situation, causing a spell of runaway inflation in Japan.

The Americans took advantage of the Japanese aversion to currency appreciation, spooking the foreign exchange market with hints that the yen was headed up as a tool to achieve their objectives in bilateral trade talks. From the 1970s into the 1980s, Japan and the United States conducted negotiations on a variety of trade issues, starting with textiles and continuing with steel, color televisions, automobiles, semiconductors, and other items, with Washington repeatedly winning Tokyo’s agreement to rein in Japan’s exports and increase its imports from the United States. US pressure for a stronger yen was a consistent theme throughout these talks.

The Plaza Accord and Japan’s Spectacular Bubble

Fast forward to 1985: On September 22, at the invitation of US Treasury Secretary James Baker, the finance ministers and central bank governors of the Group of Five (Britain, France, West Germany, Japan, and the United States) met at the Plaza Hotel in New York, where they reached an accord on lowering the value of the dollar. Under the administration of President Ronald Reagan, inaugurated in 1981, the Federal Reserve Board, headed by Chairman Paul Volcker, had severely tightened monetary policy to rein in inflation. The resulting rise in interest rates had caused funds to pour into the United States, thereby pushing up the value of the dollar. Fearing that the strong greenback would cause the US trade deficit to swell further, Washington pushed for joint intervention in the foreign exchange markets by the G5 countries to bring the dollar down.

At the time of the Plaza Accord the yen was trading at about ¥240 to the dollar. Japanese Finance Minister Takeshita Noboru apparently expected it to settle at a rate of about ¥200, a rise of 20% against the dollar, in the wake of the agreement. But the yen kept climbing, roughly doubling in value over the following three years. Japan’s monetary authorities intervened massively in the foreign exchange market, buying dollars in an attempt to resist the yen’s rise. The Bank of Japan cut its policy interest rate five times, bringing it down to a historic low of 2.5%, a rate that it maintained for over two years. On the fiscal policy front, the government implemented public works and other forms of spending to counter the contractionary effect of the yen’s strength.

Under this policy mix, financial markets were flooded with money, and though consumer prices held steady, the prices of stocks and land ballooned, resulting in what French economist Thomas Piketty identified as “the most spectacular bubble in the period 1970–2010” in his Capital in the Twenty-First Century.

Deflation Depresses Japanese Wages

The bubble of the late 1980s collapsed at the beginning of the 1990s, first in the stock market and then in the market for land. The plunge in asset markets left banks and other financial institutions holding large amounts of bad loans. And in the latter part of the decade, while institutions were still struggling to clear these nonperforming assets from their portfolios, they were hit by the effects of the Asian financial crisis of 1997. Over the quarter century since then, the Japanese economy has been experiencing a prolonged bout of deflation, with the result that the prices of goods and services are low by comparison with other leading countries. The surge in inbound tourism in the years before the coronavirus pandemic has been explained as resulting from the attraction of Japan’s competitively low prices for hotel accommodations and restaurant meals. Our country has come to be called “cheap Japan.”

Japan’s purchasing power has also fallen. In foreign markets for prized food items, such as crabs, Japanese buyers increasingly find themselves outbidden by competitors from emerging nations. This is only to be expected inasmuch as the yen’s real effective exchange rate, which reflects purchasing power, is less than half of its 1995 peak and has declined 30% since 2010.

In addition, the wages paid to Japanese workers have declined in relative terms. According to data from the Organization for Economic Cooperation and Development, Japan’s average annual wages (based on purchasing power parity) came to $38,600 in 2019. This was the lowest figure among the Group of Seven leading economies, amounting to less than 60% of the US figure, $65,800, and slightly more than 70% of Germany’s $53,600.

Excessive Fear of a Strong Yen

Back in 1985, the year of the Plaza Accord, Japan was the world’s biggest exporter of manufactured goods. Policymakers at that point should have been thinking about the prospects for this country as the “world’s factory” in a strong-yen environment. But the government, which took the yen’s rise as a national crisis, focused its attention on stimulating domestic demand with huge fiscal outlays, mainly for public works. As a result, employment in the construction industry grew from 5.30 million in 1985 to a peak of 6.85 million in 1997.

If the authorities had redirected some of this massive spending to the development of human resources in the field of information technology, including support for the training of software engineers and for the setting up of new enterprises, the outcome might have been quite different. Note that Amazon and Google were founded in the 1990s, Facebook in 2004. Perhaps Japan could have given birth to a global IT platform company of its own.

A strong yen is disadvantageous for Japanese exporters, but it means lower prices for Japanese consumers and lower costs for Japanese traveling abroad. The currency policy that the authorities adopted—one of seeking to avert the rise of the yen rather than taking advantage of it—was a failure, turning our country into “cheap Japan.”

Half a century ago, then Emperor Hirohito is said to have suggested that revaluation would be a good thing, raising the international standing of the yen. Will the day come when the people of Japan share this view?

(Originally written in Japanese. Banner photo: US President Richard Nixon delivers a televised address to the nation on August 15, 1971, announcing major economic policy changes, including the suspension of the dollar’s convertibility to gold. © AP/Aflo.)