Market Jitters Grow over Takaichi’s “Proactive” Fiscal Agenda

Economy Politics- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

The High Cost of Cutting the Consumption Tax

Growing anxiety over Japan’s fiscal deterioration pushed up long-term interest rates to 2.2% in January 2026, jumping from 1.1% in early 2025. The government had been edging closer to achieving a primary budget surplus—its benchmark for fiscal health—in fiscal 2025 and 2026. The Takaichi Sanae administration’s decision to accelerate cross-party discussions on reducing the consumption tax on food, however, risks derailing that progress.

If the prime minister follows through on her pledge to cut the food tax rate to zero, the resulting revenue shortfall would reach ¥5 trillion per year, wiping out any prospect of a primary surplus. Takaichi has stated she will not issue deficit-financing bonds to cover the gap, but if the tax cut is implemented early in fiscal 2026, which begins in April this year, a funding shortfall could be unavoidable.

Bond markets appear increasingly nervous about Japan’s return to an era of chronic deficits. Reflationists insist that the goal of a primary surplus has only slightly been delayed, but markets had already priced in an imminent surplus. When expectations change, interest‑rate projections shift with them—hence the jump to 2.2%.

Japan’s credit default swap spreads, which reflect sovereign credit risk, have risen sharply since December 2025. This suggests not a temporary supply-demand imbalance but a deeper erosion of confidence in Japan’s fiscal position.

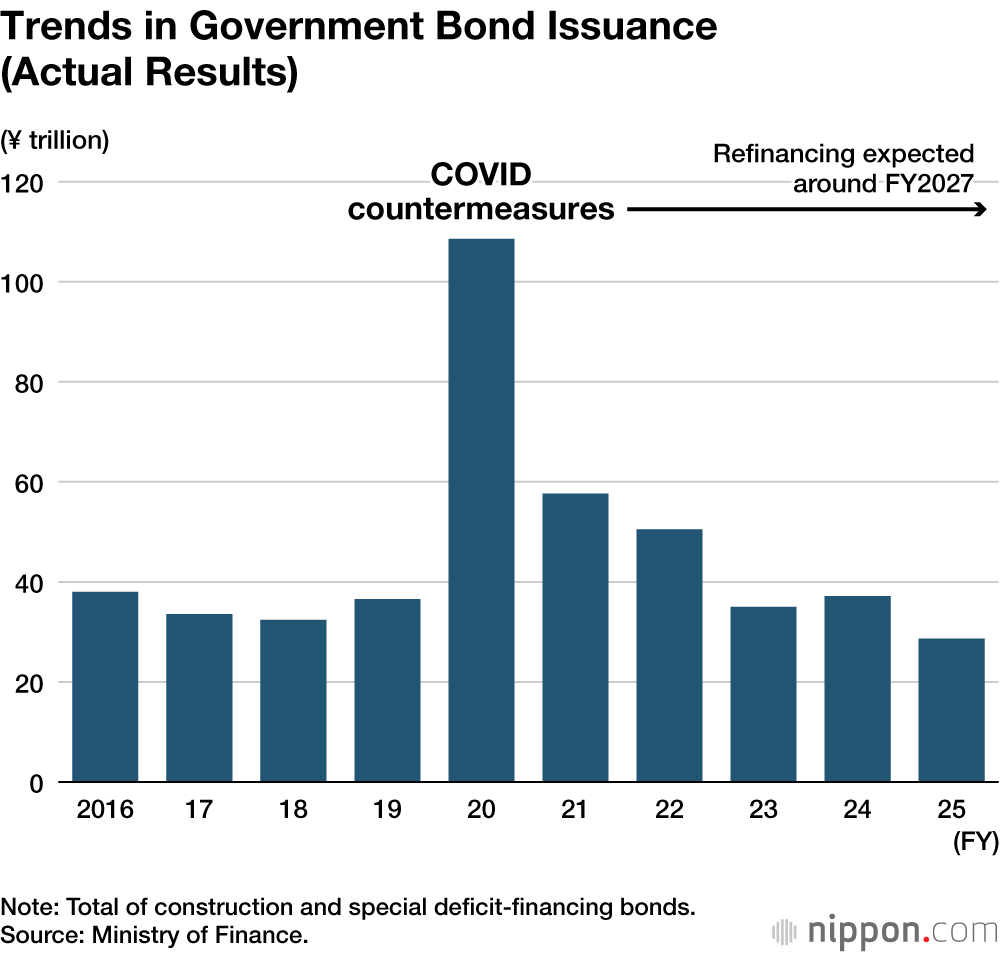

A Looming Wall of COVID-Era Debt

Another reason for the urgency in restoring a primary surplus is the need to refinance the huge volume of bonds issued in 2020 during the COVID-19 pandemic.

Fiscal 2026–28 had been expected to be a period when new issuance could be reduced. Instead, the Takaichi administration appears intent on expanding public debt, which will drive up interest payments.

The average maturity of Japanese government bonds is seven years, so the tranche issued in fiscal 2020 will soon come due for refinancing. From this perspective, interest rates during fiscal 2026–28 should ideally remain as low as possible, as they were from fiscal 2020 to 2025. Takaichi’s policies risk squandering that advantage, however, as rising long-term rates threaten to eat into any natural revenue gains.

Until recently, Japan was on course to achieving a primary surplus and gradually reducing its debt burden. But that likelihood appears to be fading, as ballooning interest payments threaten to constrain fiscal management. Claims that the surplus target has only been slightly delayed fail to appreciate the delicate balance of Japan’s bond‑management framework.

Markets Brace for Spiraling Inflation

Concerns about inflation are also intensifying. The stock market surged after the Liberal Democratic Party captured a two‑thirds lower house majority in the February 8 general election, with investors anticipating a long Takaichi tenure and continued fiscal expansion.

The prime minister is likely to compile a large supplementary budget in autumn 2026 to stimulate growth and advance her flagship “responsible and proactive” fiscal policy. But if new investments in her 17 designated priority areas focus mainly on defense spending and public works, they will do little to increase the private sector’s supply capacity. Demand will outpace supply, pushing inflation higher, and real GDP will struggle to rise even as nominal GDP grows.

In response to such expectations, markets have moved into a pattern of higher stock prices, a weaker yen, and rising long-term interest rates. On the surface, the economy appears to be expanding, but real growth is minimal. One need not be an economist to see that fiscal stimulus during an inflationary phase will only fuel further price increases. Unfortunately, the prime minister’s advisers do not seem willing to point out these basic economic realities. No one dares to say that her thinking remains shaped by policies born in the era of deflation.

Signs of inflation are clearly visible in the widening gap between nominal long-term yields and inflation-linked bond yields. This gap, known as the break-even inflation rate, has been rising since November 2025, according to the Japan Bond Trading Co.

The Ascent of Tax‑Cut Populism

Takaichi’s aggressive fiscal stance is not the only factor behind steadily rising long-term interest rates; many opposition parties, too, campaigned on consumption tax cuts in the recent election. These proposals would lead to significant revenue losses: ¥5 trillion if the preferential 8% rate on food is slashed to zero, ¥15 trillion if the consumption tax rate as a whole is halved, and ¥31 trillion if the tax is abolished entirely.

Takaichi promised to eliminate the tax on food purchases for just two years, but reinstating the levy in an inflationary environment will be politically impossible. Even with a landslide victory, the administration lacks the political capital to do so. My prediction is that once the rate goes down, it will never be restored.

A lower tax will result in primary deficits for years, both nationally and locally. Takaichi has stated that decisions on the consumption tax will be entrusted to a national council comprising both ruling and opposition lawmakers, with implementation targeted for fiscal 2026. Proposals to apply preferential rates to items beyond food—such as energy or education-related expenses—could also gain traction. My fear, therefore, is that introducing exemptions for food risks crossing the Rubicon: Once in place, there will be no going back.

Parties may soon compete to devise ever-cleverer tweaks to win over taxpayers’ votes. This wave of tax-cut populism was triggered by the call by the Democratic Party for the People to raise the income tax threshold, which has tended to encourage part-time workers to limit their hours to stay below the ceiling.

Psychology offers a useful analogy: the famous Stanford marshmallow experiment, in which young children were told they could eat one marshmallow now or wait 15 minutes to receive a second. Those who could wait longer for preferred rewards tended to have better life outcomes—evidence of self-control and foresight.

Most opposition parties can be said to have failed the marshmallow test. Japan had finally reached the point where a primary surplus was within sight, opening room for proactive spending. But they were unable to resist the temptation. A larger public debt simply shifts the burden of repayment to future generations, and signs of such growing burdens are already visible in rising long-term rates and a weaker yen.

If there is a ray of hope in the election results, it is that Team Mirai—founded just last year by AI engineer and science fiction writer Anno Takahiro and the only party to openly oppose a cut in the consumption tax—scored a major breakthrough by winning 11 seats. Whether political leaders can resist short‑term incentives and confront the long‑term costs of their choices will determine the sustainability of Japan’s public finances.

(Originally published in Japanese. Banner photo: A monitor in a Tokyo brokerage showing rising long-term interest rates, January 13, 2026. © Jiji.)

consumption tax inflation yen depreciation market Takaichi Sanae