Spring Wage Hikes Signal Shift in Japanese Economy: But Small Businesses Struggle to Meet Costs

Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Wage Hikes as the New Normal

The results of Japan’s 2026 shuntō spring labor negotiations have been encouraging. On March 18, a raft of major companies announced their decision to fully accept their unions’ wage demands for 2026. According to Rengō (Japanese Trade Union Confederation), as of March 23, the average reported pay increase for companies of all sizes was 5.26% (including scheduled pay raises)—down slightly from the figure released at the same stage last year, but still exceeding the 5% mark. Even at small and medium-sized enterprises (fewer than 300 employees), a key focus of this year’s labor offensive, the average wage increase exceeded 5%, albeit just barely. The outcome slightly surpassed the 4.69% forecast released by the Japan Institute of Labour Policy and Training in February on the basis of its survey of management, labor, and experts.

A notable feature of this year’s shuntō was the proactive stance of Japan’s major employers. This reflects the policy announced by Keidanren (Japan Business Federation) at its late-January Labor-Management Forum, which marks the official start of shuntō negotiations. Speaking at the event, Keidanren Chairman Tsutsui Yoshinobu stated, “Our basic policy is that, in the 2026 labor negotiations, management should start from the premise of an increase in base pay so as to further strengthen the trend toward wage increases that began to take hold firmly in 2025.” This suggests that business is now solidly on the same page with labor and the government in recognizing the need for ongoing wage increases. If so, the long era of nominal wage stagnation may finally be behind us.

To what can we attribute this new mindset?

One factor is the shift from a deflationary economy to an inflationary one in the years since the COVID-19 crisis. Japan’s consumer price index has risen more than 2% each calendar year since 2022 thanks to a combination of factors, including the end of hyper-globalization (which had fostered intense global price competition) and the long-term decline in the yen’s value, a result of Japan’s trade deficit. With food prices rising at an especially swift pace in recent months, substantial wage increases were needed just to keep pace with the cost of living.

Intensifying labor shortages are another factor that has helped to normalize wage increases after years of stagnation. In the Bank of Japan’s March 2026 Tankan (Short-Term Economic Survey of Enterprises in Japan), the diffusion index for employment conditions was –38, signaling a historically high percentage of understaffed companies. Japan’s plunging birth rate has affected the supply of younger workers in particular. In recent years, big corporations have taken the lead in raising wages in an effort to boost recruitment, and SMEs are being forced to follow suit in order to compete for new human resources and retain the talent they have.

Small Businesses on a Cliff Edge

For some time now, the Japanese government has stressed the need to set in motion a “virtuous cycle” of wage, price, and productivity growth. Has this goal been achieved?

Sustained wage increases were the first hurdle, and that appears to have been cleared. But higher wages alone are not sufficient. A virtuous cycle requires that wages, prices, and productivity all improve in tandem. That is not yet the case.

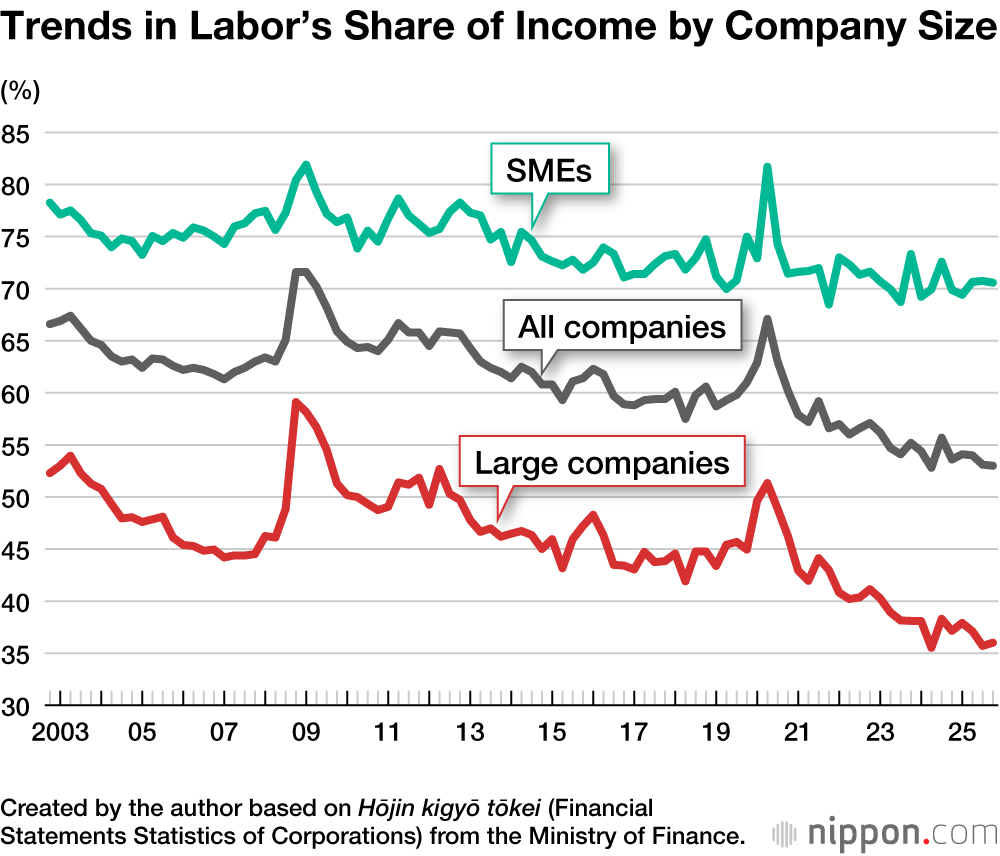

One lingering issue is the relationship between productivity gains and wage increases. As seen in the accompanying chart, labor’s share of income has been declining in recent years. This tells us that wage increases are still lagging behind productivity gains.

The chart also highlights a significant divergence between big companies and SMEs in this regard. It tells us that large corporations are primarily responsible for the overall decline in labor’s share, while SMEs are resisting that trend—even though large corporations are raising wages at a faster rate. The reason labor’s share has fallen more slowly among SMEs is that small businesses, which are hit harder by increases in the costs of raw material, are unable to pass those costs on to customers. The formula for labor’s share is gross value added divided by total labor compensation. Cost increases that are not passed on cut into a business’s gross value added, thus inflating labor’s share.

In fact, smaller companies have found it quite difficult to boost wages in recent years owing to rising materials costs and dwindling profit margins. Yet they now have little choice if they want to secure the personnel they need to operate. In the December 2025 LOBO survey (Quick Survey System of Local Business Outlook), conducted by the Japan Chamber of Commerce and Industry, the percentage of companies planning to raise their starting pay in fiscal 2026 increased by 3.1 percentage points from the year-before figure. At the same time, a full 35.5% of responding companies—up from 32.6% the previous year—said they were “raising wages defensively” even though business had not improved.

Amid such pressures, a growing number of SMEs are exiting the market, unable to adapt to the changing environment. Of course, a healthy economic system will inevitably weed out businesses that cannot compete. Smaller businesses are not exempt from the necessity of continually reviewing their operations so as to control costs as conditions change. The problem now, however, is that the economy is undergoing a historic shift, and business practices that took hold during the long era of deflation stubbornly persist, preventing the normal pass-through of cost increases now that inflation has taken hold.

The collapse of even well-run SMEs as a result of outdated business practices threatens to weaken Japan’s industrial base. To prevent that, we need to create an environment in which costs are passed on as a matter of course, while establishing programs to assist individual SMEs that run short of managerial resources.

Food and Energy Prices Are Key

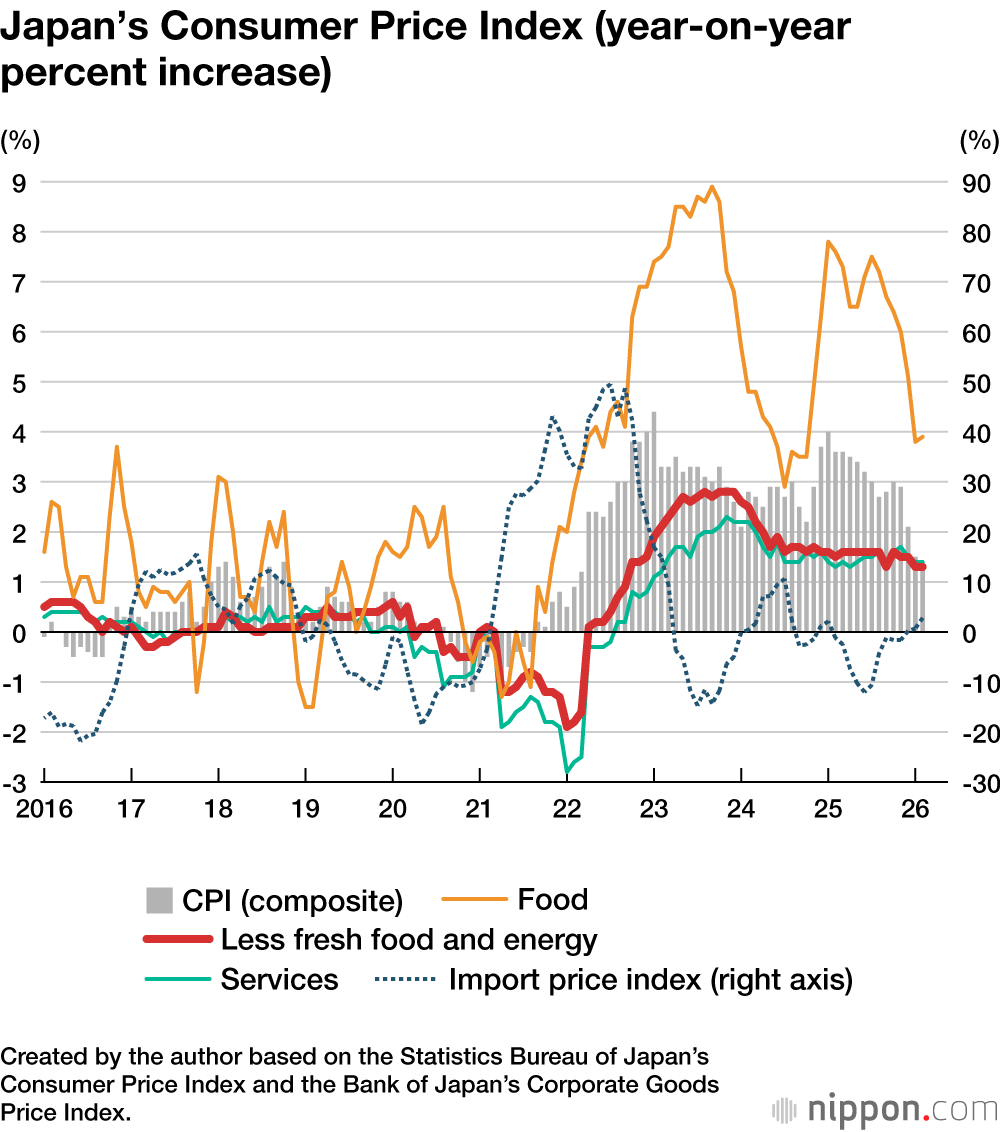

Another problem is the relationship between consumer prices and wages. There has been a good deal of focus on the long-term decline in real wages, but the issue last year—when companies offered pay increases of close to 5.5% on average—was not wages but inflation. Unlike conventional inflation, moreover, this surge in prices is limited to certain sectors, which makes it difficult to combat through fiscal and monetary policy. Food and energy costs are the main reason inflation has exceeded the central bank’s 2% target over the past few years. Since 2024, the rise in consumer prices excluding food and energy has been below the target rate of 2%.

Because fresh food and energy prices are affected by short-term weather conditions and global market fluctuations, it is common to exclude those items when calculating the underlying inflation rate. The US Federal Reserve calls this “core inflation.” One reason the Bank of Japan has been hesitant to raise interest rates is that, when food and energy are excluded, inflation is below the target rate of 2%. But given that food prices have been rising continuously for the past few years, we can no longer dismiss this as a transient problem.

The basic cause of Japan’s soaring food prices is that global food supply is struggling to meet demand owing to such long-term factors as climate change and the growth of the emerging economies. Climate change is increasing the frequency of droughts, wildfires, and floods. Moreover, the strain on ecosystems is contributing to outbreaks of avian influenza and other livestock diseases. The result is increasing instability in the global supply capacity at a time of surging demand caused by the growth of the emerging economies worldwide.

Meanwhile, oil and gas prices have skyrocketed amid the Middle East turmoil triggered by the US and Israeli attack on Iran, and it is uncertain when or if they will return to prewar levels. Even if the fighting ends and the traffic through the Strait of Hormuz returns to normal, it will take time to rebuild the energy infrastructure that has been destroyed in the Gulf states. Furthermore, oil-consuming countries will be anxious to replenish the reserves that they tapped during the crisis, placing additional strain on energy markets.

Japan is highly dependent on imports for both food and energy. As the costs of these imports rise, so will our trade deficit. A growing trade deficit could weaken the yen even more, which would inflate Japan’s trade deficit further in a kind of vicious circle. All of this has the potential to exacerbate inflation driven by food and energy prices. If crude oil settles at $100 per barrel and Japan experiences another surge in food prices like the one it faced in 2025, then inflation could rise to 4%–5%.

When inflation rises, companies need to raise wages even faster to achieve real growth. If the inflation rate were to hit 4%–5%, an average wage increase of at least 6%–7% (including scheduled pay raises) would be required to boost disposable income. For the many small companies that are unable to pass on the full burden of cost increases, this would be a bridge too far.

Don’t Obstruct the Virtuous Cycle

The current energy crisis is a classic example of an exogenous shock. In such a situation, the correct response is for economic entities to share the burden of higher costs while staying focused on long-term goals. In concrete terms, this means maintaining wage increases at around 5% while promoting cost pass-through to prevent undue strain on Japan’s SMEs.

Japan’s consumer price index remains low for goods and services outside the food and energy sectors. Under the circumstances, fiscal or financial policies designed to curb price increases overall could prove counterproductive in terms of promoting cost pass-through. Where food and energy prices are concerned, the emphasis should be on direct relief for the lower- and middle-income households most heavily impacted, rather than on industry subsidies or other blanket measures aimed at reducing prices.

In addition, given the prospect of relatively high food and energy prices over the medium-to-long term, the government needs to accelerate agriculture and energy policies geared to boosting self-sufficiency. From this perspective as well, cost-controlling subsidies should be avoided, as they reduce the economic incentive to increase self-sufficiency.

The results of the 2026 shuntō seemed to herald a new era of steady nominal wage growth, driven by changes in the global economy and Japan’s population structure. With government, labor, and industry all in basic agreement on the need for substantial annual increases, a virtuous cycle of economic growth seemed within reach. Unfortunately, it was at that very moment that the latest conflict in the Middle East broke out, injecting a new element of chaos and uncertainty into the equation.

Rather than let ourselves be thrown off course by this disturbance, we must keep a firm hand on the tiller. It is vital that labor and management stand united in their commitment to maintain annual wage increases of around 5%. The government, meanwhile, must avoid shortsighted measures that could disrupt the virtuous cycle. Instead, it should treat the current crisis as an opportunity to launch structural reforms geared to boosting Japan’s food and energy independence. In the medium-to-long term, this is the best way to counter the global forces of food and energy inflation, facilitate real wage increases, and sustain a virtuous cycle of economic growth.

(Originally published in Japanese on April 15,2026. Banner photo: An official of the Japanese Association of Metal, Machinery, and Manufacturing Workers records the results of spring wage negotiations at the labor federation’s headquarters in Minato, Tokyo, on March 18, 2026. © Jiji.)