Fiscal Policy on the Brink: Rising Inflation, Weaker Yen Put Pressure on Takaichi

Politics Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Caught in a Fix, Barely Half a Year In

Prime Minister Takaichi Sanae’s Liberal Democratic Party swept February’s general election in a landslide, enabling it to solidify its political base. Market sentiment, however, tells a different story.

Economic security is the Takaichi administration’s top priority. But the sudden outbreak of the Iran War at the end of February has plunged the world into another “oil‑shock.” Japan’s longstanding vulnerabilities in energy and economic security have erupted into full view, forcing the government, ironically, into a reactive scramble toward “economic security” itself.

The fiscal 2026 budget cleared the National Diet only on April 7—already several days into the new fiscal year. Rising interest rates and a weakening yen, meanwhile, have raised the specter of stagflation. Barely half a year after taking office, the administration’s fiscal management already appears to be on the brink, and any misstep could prove fatal.

A Fiscal Stance Under Intensifying Scrutiny

True to its “proactive” stance, the administration has pushed through an ¥18 trillion fiscal 2025 supplementary budget, followed by a record‑setting ¥122 trillion fiscal 2026 initial budget. Although the supplementary package included some inflation relief, a substantial portion of its funding—around ¥12 trillion—will be covered by newly issued government bonds. The fiscal 2026 initial budget, meanwhile, places its emphasis on investment incentives aimed at realizing the administration’s vision of a “strong economy.”

The Takaichi administration argues that as long as the debt‑to‑nominal‑GDP ratio is trending downward, fiscal policy remains “responsible” and presents no problem. This effectively sidelines Japan’s longstanding commitment to improving the primary balance in line with other major economies. It also means that little effort is being made to tackle inflation, which has imposed real hardship on households, or to address a key underlying factor by stabilizing the weakening yen. It is almost as if the administration welcomes inflation, since it boosts nominal GDP and lowers the debt ratio, thereby making fiscal expansion easier.

During a February 2026 policy speech to a special session of the Diet, the prime minister even described past fiscal management as “excessively austere,” despite Japan’s debt‑to‑GDP ratio hovering around 230% (as of October 2025, according to projections by the International Monetary Fund)—the highest among developed economies. Her comments betray little sense of fiscal crisis.

Japan’s Hard Fiscal Reality

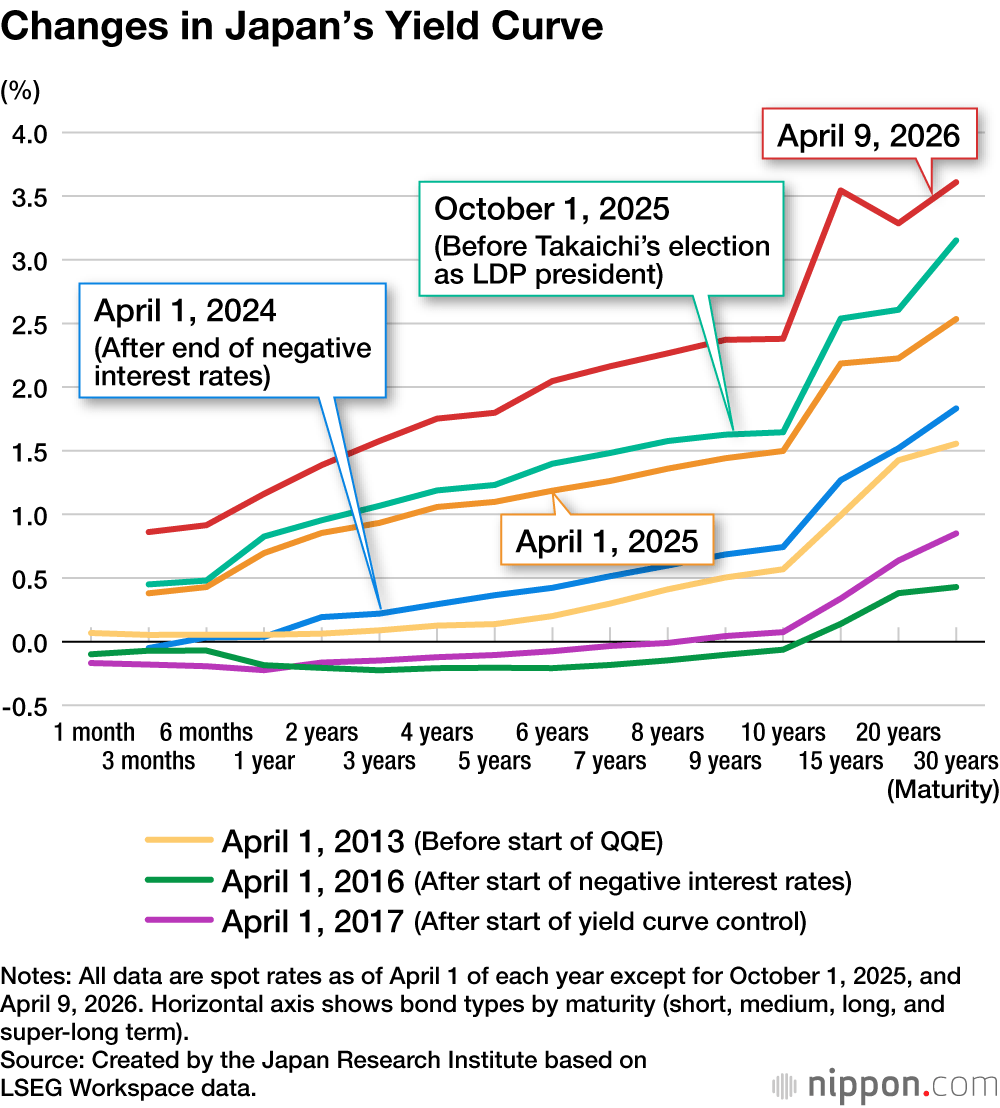

Market interest rates have risen steadily since the launch of the Takaichi administration, especially at the super‑long end of the yield curve, as shown in the figure immediately below. In June 2025, the Ministry of Finance was forced to alter its bond‑issuance plans because yields demanded by the market made super‑long bonds with maturities of 20, 30 and 40 years effectively unissuable.

To cope, the government shifted issuance toward 2‑year and short‑term bonds (treasury discount bills). But this merely postpones the problem: short‑term bonds must be rolled over quickly, increasing near-future refinancing risks. The ministry is also aiming to begin issuing floating‑rate bonds—an approach typically associated with countries approaching fiscal distress—in January 2027. This is the hard reality Japan is facing.

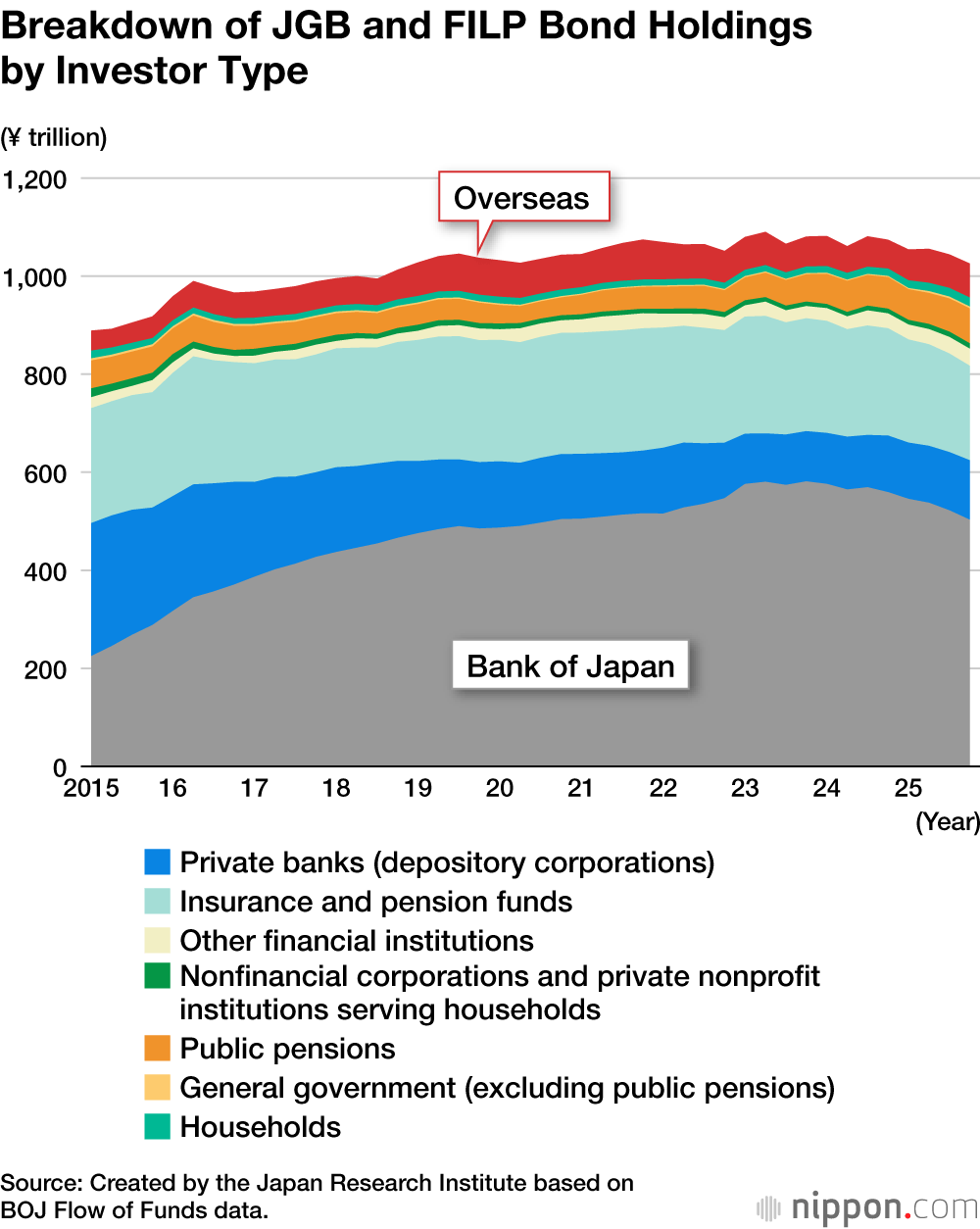

Foreign investor behavior underscores the concern. Despite rising yields and Japan’s massive bond market, overseas holdings of medium- to long-term Japanese government bonds have barely grown, as seen in the trend chart below. Investors appear wary of Japan’s fiscal trajectory and unwilling to take on longer-dated risk.

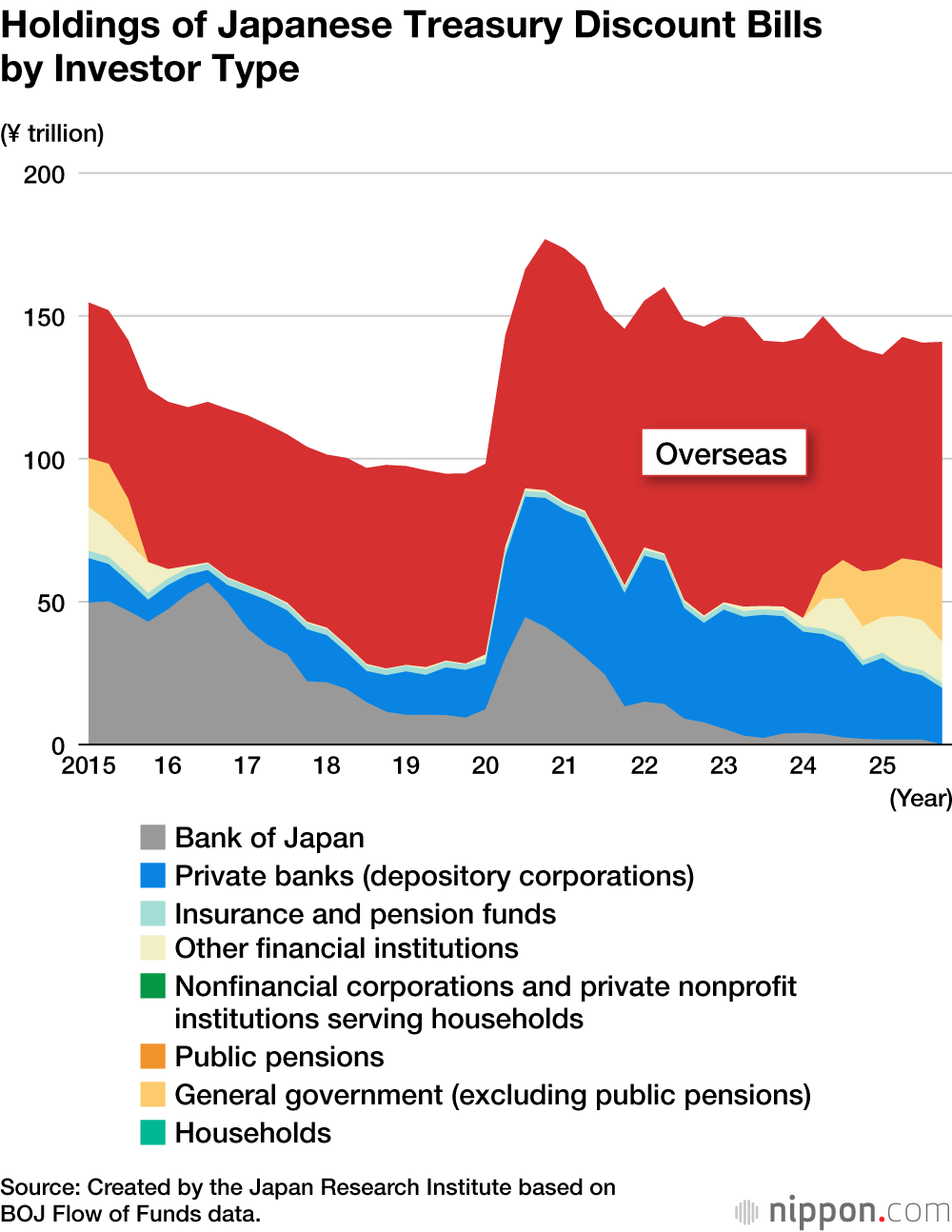

Short term JGBs of a year or less tell a different story, as foreign investors hold more than half of the market, as seen in the red portion of the following chart. But even here, holdings have plateaued. Their willingness to buy short maturities likely reflects the ability to exit quickly if Japan’s fiscal situation deteriorates. Relying on short term issuance to avoid higher coupon costs may seem convenient for now, but it risks tightening the noose around the government’s own neck.

Japan’s top fiscal priority is clear: reduce total bond issuance by improving the fiscal balance. In fiscal 2025 alone, roughly ¥149 trillion in previously issued bonds will mature. Unless the government can redeem them with tax revenue or issue the same amount in rollover bonds, Japan could face default. Given this reality, the fact that new bond issuance in the fiscal 2026 budget was kept under ¥30 trillion offers little comfort.

Difficult Decisions Ahead

In her Diet statements and elsewhere, Prime Minister Takaichi has insisted that she will not pursue “reckless” fiscal management. But one wonders whether she fully understands what this requires. A series of unavoidable fiscal challenges is already bearing down on the government.

The first is the need to respond to surging oil prices. The administration plans to offset higher costs by using contingency funds from the fiscal 2025 and 2026 budgets, but these will likely be depleted in a few months. If the Iran War continues to disrupt passage through the Strait of Hormuz, a supplementary budget early in fiscal 2026 may become unavoidable. But how will it be financed?

Discussions by the National Council on Social Security have begun on tax reforms to introduce refundable tax credits and to slash the consumption tax on food for two years. Will the government be able to secure the roughly ¥5 trillion per year in stable revenue needed to support such measures?

International markets will be watching closely when the Basic Policy on Economic and Fiscal Management and Reform (honebuto no hōshin) is released in June. The administration is arguing that it will be enough for the government to achieve the primary balance target several years later, not in a single year. But that sort of argument seems to me to make no sense. Takaichi’s signals that the government may ease its commitment to the primary balance target could effectively amount to shelving it.

Japan faces a stream of difficult decisions that will determine the course of its fiscal future. Global financial markets are likely to react quickly to whatever steps the Takaichi administration takes. The experience of the European debt crisis more than a decade ago offers a reminder that once confidence in a country’s fiscal management begins to falter, markets can move with astonishing speed. It is a lesson Japan would do well to keep in mind.

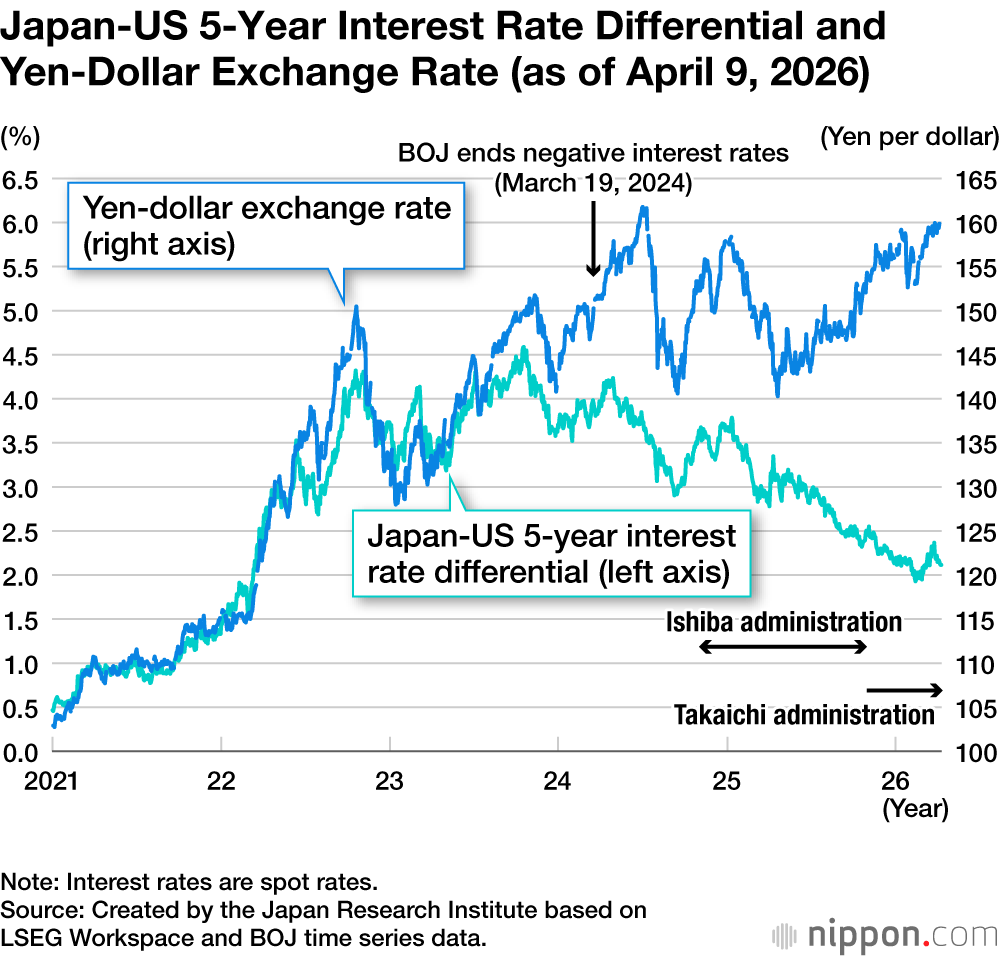

The recent yen depreciation can no longer be explained by interest rate differentials alone and suggests that market confidence in Japan is beginning to waver, as made clear in the following chart. If tensions in the Middle East persist, Japan’s economic security vulnerabilities could push the yen even lower.

To contain inflation and stabilize the yen, the administration must implement a fiscal policy capable of withstanding the rate hikes the BOJ needs to execute. That means adhering to the primary balance target, laying out a credible path to an early primary surplus, and engaging seriously in tax increase debates.

Japan must confront the hard truth that the illusion of fiscal improvement can no longer be maintained through inflation or nominal growth. Without fiscal discipline, the country’s deteriorating public finances could become the Takaichi administration’s fatal undoing.

(Originally published in Japanese on April 21, 2026. Banner photo: Prime Minister Takaichi delivering a policy speech to the House of Councillors, February 20, 2026. © Reuters.)