An Abenomics Report Card: What Did It All Mean?

Politics Economy- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

Employment Rises, But What Kind?

The “three arrows” of the Abenomics economic strategy unveiled by Prime Minister Abe Shinzō soon after he took office in late 2012 are an aggressive monetary easing policy aimed at pulling Japan out of deflation, flexible application of fiscal stimulus, and a growth strategy for sparking vigorous private-sector investment. Of these, monetary policy attracted the most attention. Kuroda Haruhiko, who took over as Bank of Japan governor in March 2013, pursued monetary easing of a “different dimension,” effectively bringing about a fall in the value of the yen and rising share prices that made it seem like the Japanese economy was roaring back to life.

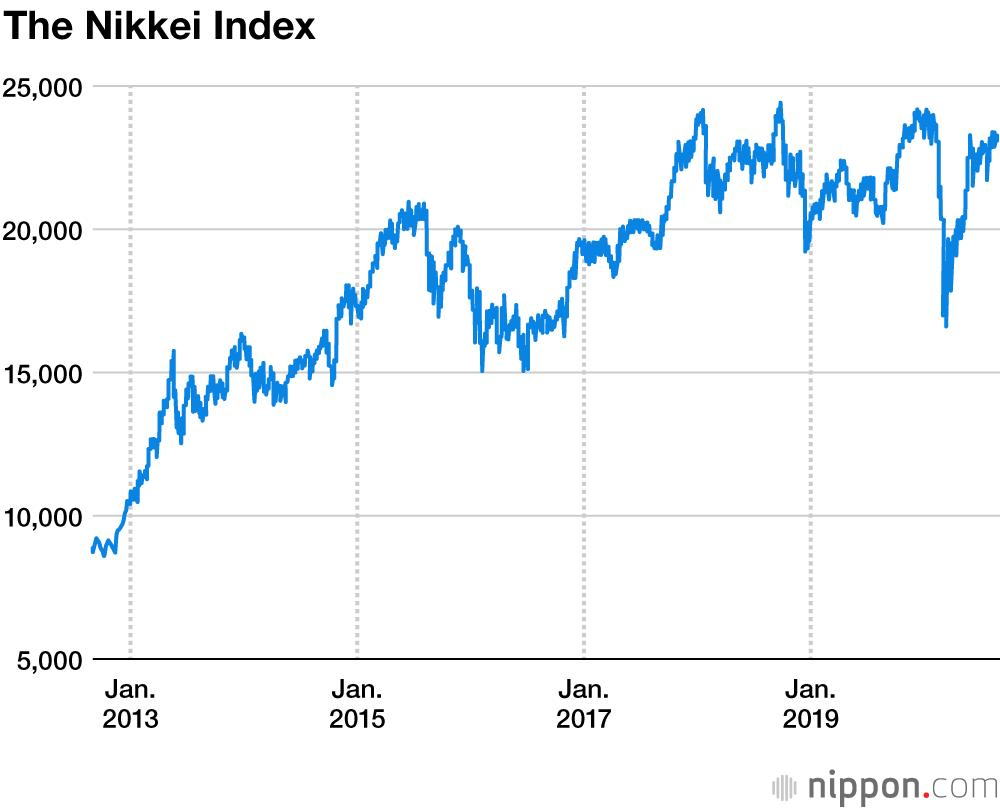

Indeed, the Nikkei index nearly doubled from the end of 2012, when Abe began his second term in office, through the end of 2019, just before the COVID-19 pandemic exploded worldwide. The yen, too, fell considerably against the US dollar, as seen below. Unemployment in Japan, meanwhile, which was above 4% at the end of 2012, went as low as 2.2% just before the pandemic. Prime Minister Abe proudly noted at the August 28 press conference where he announced his upcoming resignation that on his watch, more than 4 million jobs had been created.

The Japanese Economy Looks Good

| 2012 | 2019 | 2020 | |

|---|---|---|---|

| Yen-dollar rate | ¥85 (as of Dec. 26) | ¥109 (as of Dec. 30) | ¥105 (as of Aug. 31) |

| Real GDP growth (on annual basis) | –3.5% (Jul.–Sep., revised) | 1.80% (Jul.–Sep., revised) |

–27.8% (Apr.–Jun., preliminary) |

| Unemployment | 4.2% (Dec.) | 2.2% (Dec.) | 2.8% (Jun.) |

But this glosses over a multitude of problems. The rise in the working population is due to a dramatic rise in nonregular workers, many of whom are at risk of losing their jobs when they are hit hard by a crisis like COVID-19. Real wages, meanwhile, have actually declined on average, and little has been done to address the growing economic gaps in society, leaving the number of people receiving welfare assistance of some kind consistently high.

Moreover, Governor Kuroda’s vaunted goal of hitting the 2% inflation mark in consumer prices within two years has yet to be reached, seven years on. Today the Bank of Japan holds nearly half of all outstanding Japanese Government Bonds after buying them steadily in its ongoing bid to drive prices upward.

Other Economic Indicators

| 2012 | 2019 | 2020 | |

|---|---|---|---|

| Real wage index | 103.8 (Dec.) | 99.1 (Dec.) | 98.2 (Jun.) |

| Nonregular workers | 18.27 million (Dec.) | 21.96 million (Dec.) | 20.44 million (Jun.) |

| Consumer price index | –0.2% (Dec.) | 0.7% (Dec.) | 0.0% (Jul.) |

| Households receiving welfare assistance | 1.57 million (Dec.) | 1.64 million (Dec.) | 1.64 million (May) |

By the end of his term in office, Prime Minister Abe was paying very little attention to the CPI; rumors were flying in Kasumigaseki, home to Japan’s central bureaucracy, and Hongokuchō, where the central bank is located, that he had in fact told BOJ officials who met with him at the Kantei, the prime minister’s official residence, that “price indices are no longer something to worry about.” According to one disgruntled official who was involved in monetary policy, “They talked at first about a ‘different dimension’ of easing, but in the end, we had the ladder pulled out from under us.”

Indeed, especially once the coronavirus pandemic rolled around, the central bank’s ultraloose monetary policy was functioning as little more than a debt monetization measure supporting the issuance of massive levels of government bonds.

Three Governance Patterns

When we look at the way that decisions were reached in putting together the Abenomics strategies, we can find three main patterns. The first of these is one where the prime minister and his confidantes lead the decision-making process. This was the pattern most in evidence during Abe’s record-breaking tenure.

“Confidantes” here means more than just the prime minister’s secretaries and close advisors. It signifies more of a brain trust including economists, former Finance Ministry officials, and others with personal connections to him. These figures, along with a coterie of politicians close to Abe, formed an insider group that crafted policy.

In addition to this close group of confidantes, a handful of officials from the Ministry of Economy, Trade, and Industry were deeply involved in crafting the “three arrows” of Abenomics. In the autumn of 2015, the “three new arrows” of the second Abenomics round were put together in the same way, resulting in the declaration of the target of ¥600 trillion in nominal growth domestic product before anyone in the senior circles of the Cabinet Office, which should have been in charge of hammering out plans like this, knew what was afoot.

Also involving only a small number of figures close to Abe were his decisions to postpone the hike in the consumption tax from 8% to 10%. In November 2014, when the first delay was decided, the administrative vice minister of finance—the highest-ranking bureaucrat in the ministry—apparently considered quitting in protest at the one-sided way this notice was delivered.

Toward the end of Abe’s administration, decisions taken in response to the expansion of COVID-19 infections also followed this first pattern. These included the distribution of “Abenomasks,” washable cloth masks sent to every household in the country, and the cancellation of in-person classes at all elementary, junior high, and high schools nationwide.

The ultimate example of this first pattern may have been the January 2013 joint statement by the government and the Bank of Japan on ways to break out of deflation and boost the economy. This document was the bank’s first admission that it would set an inflation (price stability) target, but when it came to the timeframe for its achievement, the prime minister pressured the bankers not to hedge with promises of results over the “longer term.” Abe is said to have personally instructed the Finance Ministry and Cabinet Office officials negotiating with the BOJ in this matter, basing his demands for bold monetary policy on input from proponents of reflation among his inner circle. The bureaucratic officials merely handled the details of negotiation; it was the Kantei calling the shots throughout.

Following a series of national election victories for Abe’s Liberal Democratic Party during his term, this first decision-making pattern, with the Kantei as the sole strong player, became a fixture of the Japanese system. One feature of this pattern, though, was the way that it frequently skipped fine-grained discussion of the details by experts in the relevant ministries. One official warned of the danger of this approach: “The selection of the nation’s policies is taking place within an extremely narrow band of policymakers.”

A Second Pattern: Spontaneous Bureaucratic Involvement

The second pattern of decision making during the Abe administration was one joining him with officials from the bureaucracy in a more spontaneous manner. The “spontaneous” participation by members of officialdom tended to involve people who, although they were not particularly close to the prime minister, found themselves unable to remain passive bystanders and provided their advice to him or his close associates, or leapt into the fray and played a coordinating role of some kind. The classic example of this second pattern was the 2013 negotiations between the government and the business world regarding wage hikes.

As noted above, the first Abenomics arrow of bold monetary policy received the most attention, but if it succeeded in bringing about price inflation without being accompanied by rising salaries for Japan’s workers, it would only make the lives of the people that much harder. Many bureaucrats realized this early on.

Officials from the Cabinet Office and Finance Ministry, along with Cabinet Secretariat personnel including an assistant chief cabinet secretary, “spontaneously” stepped up to offer support to the prime minister. They did so by attempting to convince business and labor leaders of the need for higher wages to accompany higher prices, in the end establishing an official council bringing government, labor, and business management representatives together to help bring about a virtuous cycle of wage hikes and price increases in the economy. They thus succeeded in bringing the business world into the process, although it did not play out so successfully on the wage front—nominal wages in 2019 shrank for the first time in six years.

Pattern Three: Specific Political Players Enter the Picture

The third pattern was one we might describe as coupling the prime minister with specific political forces. Here the prime example is the introduction of a reduced tax rate for certain items as part of the October 2019 rollout of the 10% consumption tax rate. The consumption tax is fundamentally regressive, impacting society’s weaker members most heavily. The Ministry of Finance came up with a plan to make use of the My Number taxpayer identification scheme to reduce this impact, but Prime Minister Abe threw out this proposal, replacing it with the reduced tax rate. Behind this decision were factors like the campaign pledge by junior coalition partner Kōmeitō to introduce just such a scheme, along with the influence of certain commentators with the ear of the Abe administration.

Incidentally, this issue led to the October 2015 ouster of Noda Takeshi, who opposed introducing a reduced rate, as chair of the LDP’s Research Commission on the Tax System. When Abe called him with the news, he reportedly told Noda “This is not something that I want to do” before informing him that he was being replaced. It was not so long ago that it would have been unthinkable for a prime minister to lift his hand against a party figure as powerful as the head of the tax commission. When Abe proved willing to do so, a mood spread quickly through the LDP and the central bureaucracy that it would be difficult to go against this leader’s wishes, and the idea of the all-powerful Kantei was bolstered once more.

Policy Destination Unknown

How, then, should we sum up Abenomics?

Abe Shinzō first made a name for himself during the 2001–5 administration of Koizumi Jun’ichirō, a neoliberalist who proclaimed that there would be no economic growth for Japan without reform. Early on he displayed a focus on financial policies that meshed well with this neoliberalist thought. This has been noted by figures including House of Councillors member Nishida Shōji, an LDP pol close to the prime minister, who said in a July 2019 Facta interview: “Abenomics depends on a monetarism theory grounded in neoliberalism.” This branch of economic theory focuses primarily on the money supply; broadly defined, pro-reflation economists can be classified as monetarists.

Prime Minister Abe himself has also shown a strong deregulatory streak, stressing his desire to serve as “the head of the drill breaking through the bedrock of regulation.”

A look at the decision-making approaches he has taken during his administration, though, makes it clear that he has paid scant attention to the appropriate relationship between the public and private spheres—one of the key aspects of neoliberalist economic policy. The strategies he deployed in dealing with the business community during the discussion of wage hikes make this clear.

In February 2013, Abe called the leaders of the business world to the Kantei, where he told them this: “The government intends to earnestly engage in labor market reforms and deregulation. It is my hope that Japan’s businesses will also consider what they can do, such as raising salaries for their workers.”

The question of whether to raise wages is a business decision of supreme importance to corporate managers. If Abe had truly been dedicated to the belief that private actors should be allowed to execute their own decisions, he would not have engaged in such blatant direct intervention in their affairs by pressing them to hike worker pay.

In his book Atarashii kuni e (Toward a New Nation), published in 2013 soon after the launch of his new administration, Abe wrote about the economic principles he aimed to implement in Mizuho no kuni—an ancient name for Japan meaning “land of abundant rice” and one he chose for its associations with a tight-knit agrarian society where there is much to share, but people stand ready to help one another in times of need. “Here there is a form of capitalism appropriate to Mizuho no kuni. It is not the capitalism driven by insatiable greed, but rather one that values morality and understands where true wealth lies.”

Having pressured the business community to raise wages, Prime Minister Abe appeared before the government-labor-management council mentioned above in late 2013. There he stated: “Thus far the government has engaged in ‘prudent intervention’ in the market. Is this not the very heart of the capitalism of Mizuho no kuni?”

A Keidanren official at that time expressed shock at these words. “After bringing that much pressure to bear, he really thought it could be called ‘prudent intervention.’” And one bureaucrat told me, “The direction of our economic policy today isn’t really clear.”

A Prime Minister Without Fixed Ideals

How could Abe propound the “capitalism of Mizuho no kuni” on the one hand and declare his desire to be the “head of the drill” breaking through regulatory bedrock on the other? Why would he accelerate liberalization in the agricultural sphere with Japan’s accession to the Trans-Pacific Partnership and its trade agreement with the United States? Do not these decisions run counter to the Mizuho no kuni ideals?

If Japan is to make the most of its latent potential for economic growth, it must improve productivity through liberalization and deregulation. But these steps result in widening gaps between winners and losers in society. On the other hand, pursuing Mizuho no kuni capitalism by seeking to close those gaps will keep productivity from rising. As if to conceal this fundamental inconsistency in his positions, Abe raised new policy banners one after another: building “a society where all 100 million people play an active role,” or “revitalizing the regions” of Japan.

I spoke to one official who told me: “Under Abe, day-to-day management became the norm on the policy front, and issues that needed to be dealt with over longer spans, like five or ten years, got put off entirely. Once we get through the COVID-19 pandemic the next leader will really be tested, I fear.”

Another former high-ranking government official adds: “The prime minister really has no firmly held ideals in the first place. His economic policies are easy to understand if you think of them in terms of their use as vote-winning ploys at election time, and his ‘breaking through the regulatory bedrock’ bit was just a convenient way to keep foreign capital, which thrives on deregulation, from fleeing Japan’s shores.”

One Finance Ministry official, however, shared this different take. “Turn the nation’s fiscal and monetary tools up to their maximum levels. Jump-start a self-reinforcing cycle of wage, consumption, and investment growth. These were the goals of Abenomics. But the coronavirus came along and brought this cycle to a complete halt before it could take full effect.”

Abe Shinzō once proudly stood before the world and urged it to “Buy my Abenomics!” At his resignation press conference, though, he spoke little about his economic policies, with the exception of mentioning the employment figures. In the end, what did Abenomics seek to accomplish? What did it achieve, and what did it fail to do? The time has come for Abe to quietly take stock of these questions himself.

(Originally written in Japanese. Banner photo: Bank of Japan Governor Kuroda Haruhiko, at left, confers with Prime Minister Abe Shinzō at a House of Councillors Budget Committee meeting on May 8, 2013. © Jiji.)