The Japanese Economy in 2024: Looking Toward Possible Post-COVID Growth

Economy Work Society Politics- English

- 日本語

- 简体字

- 繁體字

- Français

- Español

- العربية

- Русский

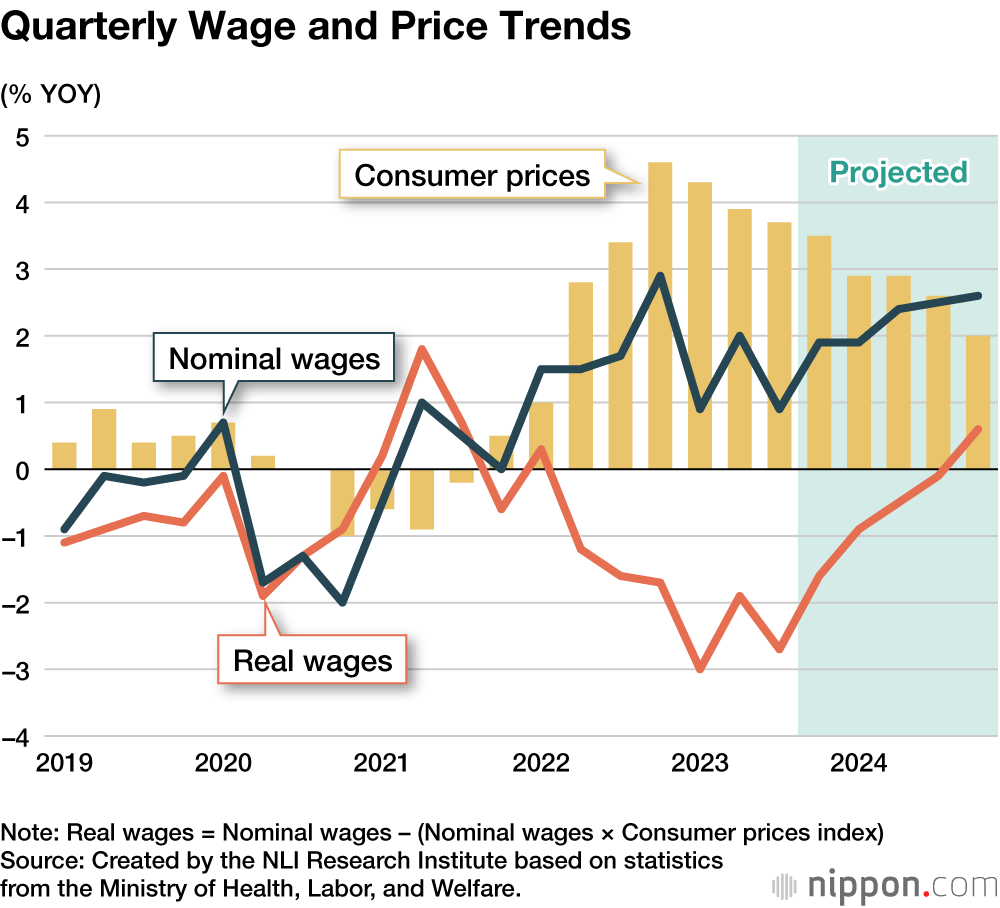

Positive Growth in Real Wages On the Way?

An important consideration in anticipating the direction of Japan’s economy in 2024 is whether prices and wages can form a virtuous economic circle. The spring wage offensive of 2023 achieved a wage increase rate of 3.6% (around 2% for base pay), an increase unmatched in 30 years. Consumer prices, however, are rising faster than the Bank of Japan’s 2% target, and the growth of real wages (growth of nominal wages discounted by the consumer price index) has been negative for more than 18 months since April 2022, year on year.

The spring wage offensive of 2024 will take place in the context of an unemployment rate trending in the mid-2% range and a tight labor market. Current profits in the Financial Statements Statistics of Corporations by Industry are at an all-time high, and consumer prices are rising at a rapid pace. It is safe to say that the environment for wage increases remains positive.

The Japanese Trade Union Confederation (Rengō), in its basic plan for the 2024 spring wage offensive, has raised its wage increase demand from around 5% in 2023 to 5% or more in 2024 (including the annual wage increase component). The Japan Council of Metalworkers’ Unions, consisting of industrial labor unions for such industries as automobiles and electrical machinery, has raised its monthly base pay demand from an increase of ¥6,000 or more in 2023 to ¥10,000 or more in 2024. In view of these developments, the wage increase rate of the 2024 spring wage offensive is anticipated to be 4.0%, a 0.4 percentage point improvement over 2023. This will be the first 4% increase achieved since 1992.

Meanwhile, consumer prices (all items excluding fresh foods) rose 4.2% year on year in January 2023, a high unseen for some 40 years. Helped in part by the government’s measures to tackle inflation, consumer prices trended at the 3% level from February through August and slowed further to the 2% level in September and subsequent months.

The current increase of prices is characterized by companies passing through to selling prices the increase of raw material costs accompanying the depreciation of the yen and the ascent of crude oil prices. This has resulted in an upsurge in the prices of goods, particularly foods. However, import prices, the main reason for the rise of domestic prices, have stabilized, and it is highly probable that the increase of goods prices will gradually abate.

Service prices, which are closely linked to wages, were slow to rise compared to goods prices. However, with the substantial increase of the wage increase rate in 2023, service prices climbed 2.1% year on year in October, an increase similar to the growth of base pay in 2023. The wage increase rate of the spring wage offensive of 2024 is expected to surpass the increase rate of 2023, and it is highly probable that service prices will continue to rise steadily.

While consumer prices will continue to climb at the 2% level for the time being, they are expected to slow to the 1% level in the second half of 2024, mainly on account of goods prices slowing their rise. While the growth rate of real wages will continue to be negative, it is highly probable that this rate will turn positive in the second half of 2024 as nominal wages accelerate their growth and as the rise of prices stabilizes.

Personal consumption is currently struggling due mainly to the decline of real wages accompanying the ascent of prices. Such consumption is foreseen to begin a recovery in the second half of 2024 supported by the effects of a tax cut and the rise of real wages.

Limited Effect for Stimulus Measures

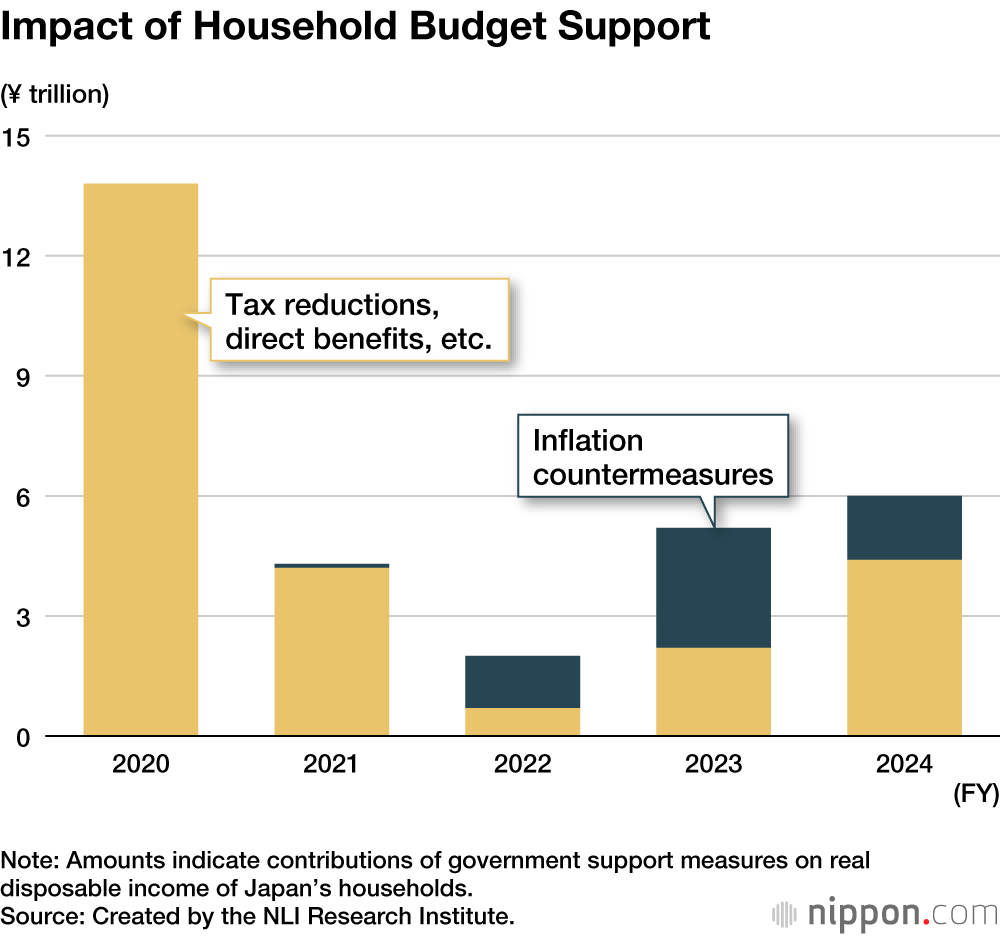

In November 2023, the government approved additional spending of ¥13.1 trillion as comprehensive stimulus measures to completely overcome deflation. The government estimates that these measures will boost real GDP by around 1.2% annually for the next three years or so. However, since supplementary budgets have decreased year on year since fiscal 2021 and since it is highly probable that the supplementary budget will not be spent in full, it is reasonable to think that the government’s estimate is excessive. In fact, a substantial ¥29.3 trillion went unspent in fiscal 2022 (consisting of ¥18.0 trillion carried forward to the next fiscal year and ¥11.3 trillion that was unused).

Meanwhile, measures to support household budgets, such as income and resident tax cuts and benefit payments to low-income persons, along with inflation countermeasures responding to the higher prices of electricity, city gas, gasoline, and kerosene, can be expected to lift the real disposable income of households. I estimate that household budget support measures will boost real disposable income by ¥5.2 trillion in fiscal 2023 (¥2.2 trillion in tax cuts and benefit payments and ¥3.0 trillion in inflation countermeasures) and ¥6.0 trillion in fiscal 2024 (¥4.4 trillion in tax cuts and benefit payments and ¥1.6 trillion in inflation countermeasures).

However, compared to increases of income viewed as permanent, as is the case with wage increases, the effect of temporary tax cuts and benefit payments in stimulating consumption is not all that large. An examination by the Cabinet Office indicates that past fixed benefit payments and regional economy promotion coupons lifted consumption by about 20% to 30% of the benefit payment. The current income and resident tax cuts and benefit payments to low-income persons will together total around ¥5 trillion. This is anticipated to boost personal consumption by about 0.4% and correspond to 0.2% of GDP.

Domestic Demand, Not Exports, Will Drive Growth

Foreign economies, on which Japanese exports depend, are highly likely to continue slowing. While the US economy has been trending firmly, a significant slowdown in the second half of 2024 is likely unavoidable from the cumulative tightening of the Federal Reserve’s monetary policy. With the termination of a zero COVID-19 policy in China, its real GDP has been predicted to accelerate from 3% growth in 2023 to the 5% level in 2024. However, burdened by a stagnant real estate market, this figure is likely instead to slow to the 4% level. Japan should not expect exports to drive economic growth during the year.

Meanwhile, reflecting the improvement of the domestic employment and income environment and the normalization of social and economic activity, personal consumption will recover centering on the consumption of services, such as eating out and travel. Capital spending will continue to grow, supported by a high level of corporate earnings. Japan’s economy is expected to continue expanding led by domestic demand.

The political situation will be a potential source of turbulence, having turned suddenly volatile toward the end of 2023 due to the surfacing of a slush fund scandal involving the Liberal Democratic Party. The ordinary session of the Diet starting in 2024 will likely be thrown into confusion. Should this come to influence the deliberation of the budget or tax reform or should the foundations of the ruling political regime become shaky, it may impact the execution of economic policies.

I predict that Japan’s real GDP will grow by 1% in 2024. This is not a particularly high growth rate, coming as it does on the heels of the economy’s sharp decline caused by the COVID-19 pandemic. However, should personal consumption increase in tandem with the growth of income, the economy’s recovery will become more readily perceived. For this to occur, the positive growth of real wages will be indispensable. What will be of greatest interest with regard to 2024 is the direction of prices and wages.

(Originally published in Japanese. Banner photos: Yoshino Tomoko, president of the Japanese Trade Union Confederation [Rengō] at left, and Tokura Masakazu, chair of the Japan Business Federation [Keidanren]. © Jiji.)